Popular Keywords

Display

News

[News] LG Display Rumored to develop Micro LED Inspection and Repair Technologies

As per a report by The Elec on March 17, LG Display has been participating since April last year in a national R&D program on Micro LED inspection and repair, led by the Ministry of Trade, Industry and Energy. The project is jointly carried out by Ulsan National Institute of Science and Techn...

Insights

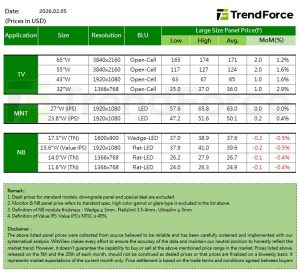

[Insights] Early March Panel Prices: TV Strength Continues; MNT Turns Up While NB Weakness Moderates

.TV Entering March, TV demand has remained stable. North American distributors have recently agreed to raise retail prices for small- and mid-sized TVs starting in the second quarter, boosting TV brands’ confidence to increase panel procurement. With demand holding steady, panel makers are al...

News

[News] Samsung Display Reportedly Weighs OLED Expansion as Apple May Plan a Second Foldable for 2027

Samsung Display is reportedly evaluating an expansion of its OLED capacity for Apple’s foldable products. According to ETNews, the company is reviewing additional investment to strengthen production capabilities not only for Apple’s first foldable iPhone but also for next-generation models, refl...

Insights

[Insights] Early February Panel Prices: TV & MNT Panels Up; Notebook Panels Down Across Sizes

.TV In February, TV panel demand is expected to stay relatively stable, while panel makers plan five to seven days of capacity adjustments during the Lunar New Year. This is likely to lower average utilization by about 10% from January, helping keep supply and demand balanced and supporting hig...

News

[News] China’s LED Industry Sees Broad Price Hikes; MLS and Kinglight Models Reportedly Up 5%–10%

China’s LED industry is seeing price hikes across the entire value chain. According to ijiwei, the latest increases span upstream chips, midstream packaging, and downstream applications, with dozens of companies issuing price adjustment notices covering products such as LED light beads, PCB boards...

- Page 2

- 30 page(s)

- 150 result(s)