Popular Keywords

Display

News

[News] World’s First Gen-8.6 OLED Production Line Enters Mass Production and Begins Shipments

As per Chosun Ilbo, Samsung Display has officially achieved mass production of Gen-8.6 OLED panels, marking the world’s first production line of its kind to reach commercial output. Sources indicate that Samsung Display has already begun paid shipments of customer-validated samples with relatively...

Insights

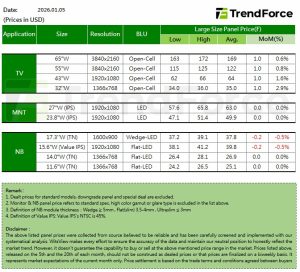

[Insights] Late-January Panel Prices: TV Panels Poised to Rise, Notebook Continue to Fall

.TV In January, despite the impact of rising memory and component prices, some leading TV brand customers continue to actively build inventory, seeking to further expand market share by leveraging their relatively stronger access to memory and other components compared with smaller brands. As a...

Insights

[Insights] Early January Panel Prices: TV Panel Prices Turn Upward, While Notebook Panel Prices Trend Lower

.TV Entering January, procurement momentum at some TV brands remains relatively strong, supporting steady TV panel demand and allowing panel makers to maintain relatively high utilization rates. With the Lunar New Year falling in February, panel makers are planning production cuts during that p...

News

[News] China’s CSOT Reportedly Set to Supply Flexible OLEDs for Samsung Galaxy A57 for the First Time

Chinese display maker CSOT is reportedly expanding its role in Samsung Electronics’ smartphone OLED supply chain. According to South Korean outlet The Elec, sources say China’s CSOT is set to supply OLED panels for Samsung Electronics’ upcoming Galaxy A57 smartphone for the first time. The Gal...

Insights

[Insights] December Panel Prices: TV Panels Expected to Rise in January on Memory Supply Concerns

.TV Since December, brand customers have increasingly viewed panel prices as having bottomed out, while also growing concerned that memory shortages and rising prices could spill over into TV products and intensify next year. As a result, some panel demand originally planned for 1Q26 has been b...

- Page 3

- 30 page(s)

- 150 result(s)