Popular Keywords

Display

Insights

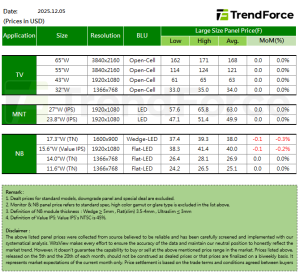

[Insights] Early December Panel Prices: Brands Increase Orders, Suggesting TV Downtrend May End Early

.TV As the year draws to a close, demand for TV panels has not cooled; instead, it remains steady and relatively firm. The main reason is that some brand customers expect panel prices to have reached the bottom and have begun increasing orders, even preparing early for 1Q26 demand. This has all...

News

[News] OLED Industry Landscape Reshapes as Chinese Companies Ramp up Investment in Expanding Production

China’s display industry is witnessing a new wave of large-scale OLED investment, with domestic panel makers pouring capital into next-generation production lines. Following TCL CSOT’s official launch of its 8.6-generation ink-jet-printed OLED line at the end of October, market data indicates th...

Insights

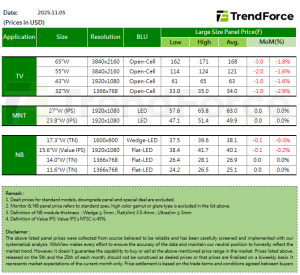

[Insights] Early November Panel Prices: TV Panels Dip as Makers Adopt More Flexible Pricing Strategies

.TV Entering November, demand for TV panels has only slightly weakened, with some brands still willing to place orders. Meanwhile, certain panel makers, aiming to hit their annual targets, have made only minor adjustments to utilization rates while actively coordinating with brand demand. As th...

News

[News] TCL CSOT Kicks Off World’s First G8.6 Printed OLED Line, Paving Way for Mass Production

China’s display manufacturers are making significant strides, showcasing growing competitiveness in next-generation panel technologies such as AMOLED. According to EE Times China, TCL CSOT’s G8.6 printed OLED production line (T8 project) in Guangzhou has officially broken ground. As the repor...

Insights

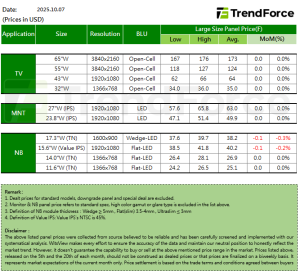

[Insights] Panel Prices in Early October: Notebook Panels Projected to Fall Slightly amid Soft Demand

.TV As year-end promotional stocking winds down and some brands begin adjusting inventories, TV panel demand is expected to gradually slow in the fourth quarter. In response to this trend, panel makers plan to adjust production during the China’s National Day holidays. China-based manufacture...

- Page 4

- 30 page(s)

- 150 result(s)