Popular Keywords

Panel Industry

Insights

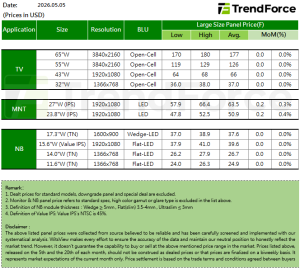

[Insights] Early May Panel Prices: TV Gains Slow; MNT Hike Momentum Moderates, NB Flat

.TV Entering May, signs of weakening overall demand have begun to emerge as some brand customers started adjusting orders, although demand for larger-size panels remains better than for smaller sizes. Panel makers have also begun implementing 3- to 5-day production adjustments during the Labor ...

Insights

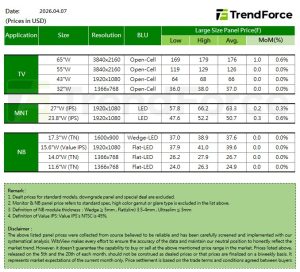

[Insights] Early April Panel Prices: Large-Size TV Panels Gain, Rising IC Costs Point to Further MNT Price Increases

.TV Entering April, some brands continue to maintain demand for TV panels, particularly for large-size segments. At the same time, component costs for panels have continued to rise, driven by war-related energy issues and semiconductor capacity crowding. As a result, panel makers are taking a m...

Insights

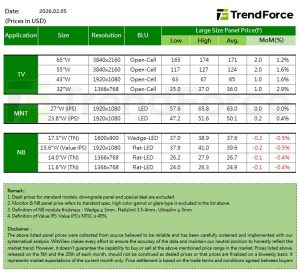

[Insights] Early February Panel Prices: TV & MNT Panels Up; Notebook Panels Down Across Sizes

.TV In February, TV panel demand is expected to stay relatively stable, while panel makers plan five to seven days of capacity adjustments during the Lunar New Year. This is likely to lower average utilization by about 10% from January, helping keep supply and demand balanced and supporting hig...

Insights

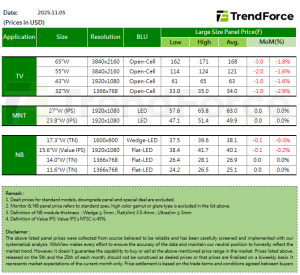

[Insights] December Panel Prices: TV Panels Expected to Rise in January on Memory Supply Concerns

.TV Since December, brand customers have increasingly viewed panel prices as having bottomed out, while also growing concerned that memory shortages and rising prices could spill over into TV products and intensify next year. As a result, some panel demand originally planned for 1Q26 has been b...

Insights

[Insights] Early November Panel Prices: TV Panels Dip as Makers Adopt More Flexible Pricing Strategies

.TV Entering November, demand for TV panels has only slightly weakened, with some brands still willing to place orders. Meanwhile, certain panel makers, aiming to hit their annual targets, have made only minor adjustments to utilization rates while actively coordinating with brand demand. As th...

- Page 1

- 14 page(s)

- 66 result(s)