Popular Keywords

Panel Industry

Insights

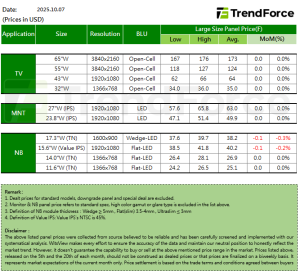

[Insights] Panel Prices in Early October: Notebook Panels Projected to Fall Slightly amid Soft Demand

.TV As year-end promotional stocking winds down and some brands begin adjusting inventories, TV panel demand is expected to gradually slow in the fourth quarter. In response to this trend, panel makers plan to adjust production during the China’s National Day holidays. China-based manufacture...

Insights

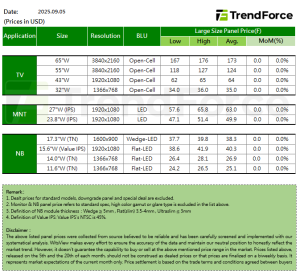

[Insights] Panel Prices in Early September: TV Expected to Hold Steady Amid Year-End Demand Prep

.TV As September begins, TV brands are preparing for year-end promotional demand, helping to sustain relatively stable momentum in panel procurement. In response, panel makers have adopted a more proactive stance in production and shipments over the past two months, easing the downward pressure...

Insights

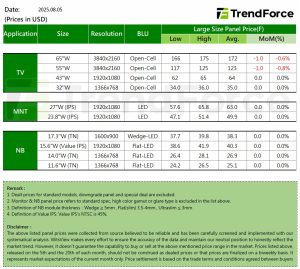

[Insights] Panel Prices in Early August: TV Panel Market Gains Momentum as Smaller Sizes Lead Recovery

TrendForce discloses the latest panel prices for early August, with details as follows. TV Entering August, TV brand clients are stocking up for year-end promotions while still hoping to meet annual targets, maintaining strong momentum in TV panel procurement. Panel manufacturers are capital...

Insights

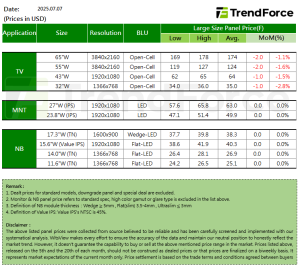

[Insights] Panel Prices in Early July: TV Panels Slightly Dip as Brands Bargain amid Weakening Demand

TrendForce discloses the latest panel prices for early July, with details as follows. TV TV panel demand remains sluggish as July begins, with some brands continuing to trim their Q3 orders to better manage inventory and gain more leverage in price negotiations with panel makers. Since Q3 st...

Insights

[Insights] Panel Prices in Early June: TV and MNT Prices Flat Amid Rising Inventories

TrendForce discloses the latest panel prices for early June, with details as follows. TV As June begins, demand for TV panels is showing signs of weakening. Since the first quarter, brand customers have been actively restocking, leading to a gradual buildup in inventory levels. Starting in t...

- Page 2

- 14 page(s)

- 66 result(s)