Tight DRAM Supply Gives Suppliers Greater Pricing Power in HBM, with HBM Contract Prices Expected to Surge Multiples Higher in 2027, Says TrendForce

Sharp increases in conventional DRAM prices since the second half of 2025 have reflected an increasingly tight supply-demand environment. However, the annual pricing mechanism adopted by the three major suppliers for HBM has prevented contract prices from fully reflecting quarterly market price increases in a timely manner, according to TrendForce’s latest research.

As the market enters 2Q26, negotiations between buyers and suppliers have shifted toward HBM4 supply agreements for 2027, which is expected to become the market’s mainstream project generation.

Based on TrendForce’s analysis of per-wafer revenue for HBM and conventional DRAM—estimated using die size, yield rates, and per-Gb pricing—HBM wafer revenue was overtaken by DDR5 64GB RDIMM in 1Q26. This has led HBM profitability to also fall below that of DDR5 64GB RDIMM since 1Q26.

Consequently, suppliers are expected to adjust production allocation between HBM and conventional DRAM depending on HBM pricing outcomes. This ensures that HBM remains the core memory component supporting AI training and inference infrastructure. The dynamic is also expected to drive broader demand across the AI ecosystem, including RDIMMs, server LPDDR, and conventional DRAM used in edge devices.

AI ASICs to drive HBM demand growth in 2026; Rubin Ultra and AI ASICs to further accelerate demand in 2027

Accelerated AI infrastructure deployment is expected to sustain strong HBM demand growth through 2026 and 2027, although the key demand drivers will differ between the two years.

In 2026, HBM demand growth will primarily be driven by AI ASIC capacity upgrades, with HBM capacity per AI chip increasing significantly from 96GB/192GB to 216GB/288GB. Although HBM capacity per GPU in NVIDIA’s Rubin platform is expected to remain similar to the previous generation, higher shipment volumes will continue lifting overall demand.

In 2027, NVIDIA’s Rubin Ultra platform is expected to further increase HBM capacity per GPU to 384GB. At the same time, AI ASIC platforms such as Google TPU are projected to further amplify HBM bit demand through rising deployment volumes.

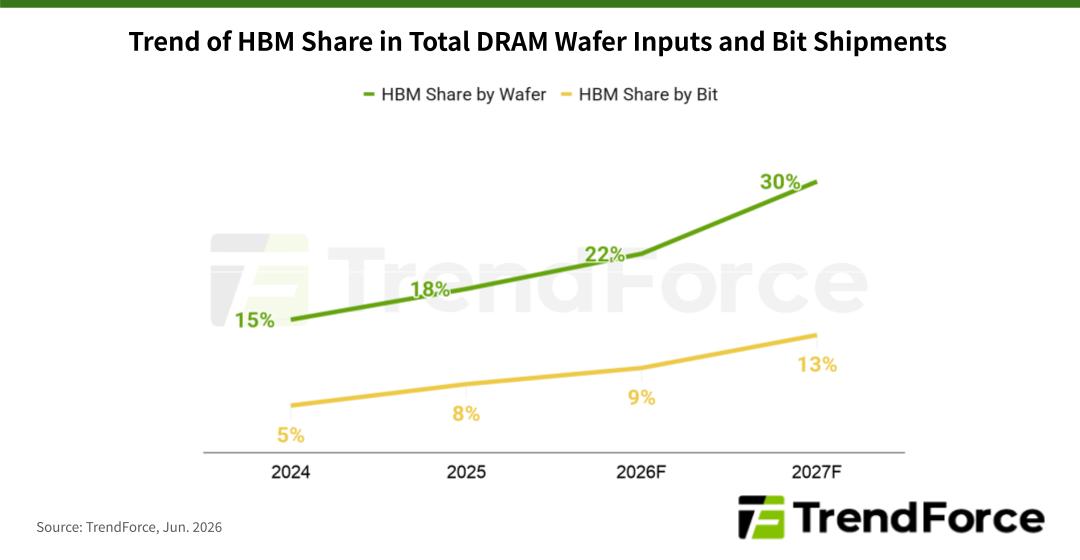

TrendForce estimates that HBM wafer input among the top three suppliers will account for approximately 18%, 22%, and 30% of total DRAM wafer input by the end of 2025, 2026, and 2027, respectively. Meanwhile, HBM bit supply is expected to represent approximately 8%, 9%, and 13% of total DRAM bit supply during the same period.

Overall, as HBM generations continue evolving in 2027, with larger die sizes and simultaneously rising demand, the crowding-out effect on conventional DRAM capacity is expected to intensify further. This will provide suppliers with strong justification for raising HBM prices and strengthen their pricing power in HBM negotiations next year.

For more information on TrendForce’s semiconductor reports and market data, please visit the Report Page, or Email (SR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.