AI Data Center Expansion to Drive Combined Monthly Capacity of EML and CW-DFB LDs to 50.7 Million Units in 2026, Says TrendForce

The rapid expansion of AI data centers and the intensifying race for AI computing power are accelerating the transition toward transmission speeds above 1.6 Tbps, according to TrendForce’s latest research. Major players such as NVIDIA, Google, and Meta are securing a stable supply by strategically locking in production capacity from electro-absorption modulated laser (EML) and continuous-wave distributed feedback laser diode (CW-DFB LD) suppliers.

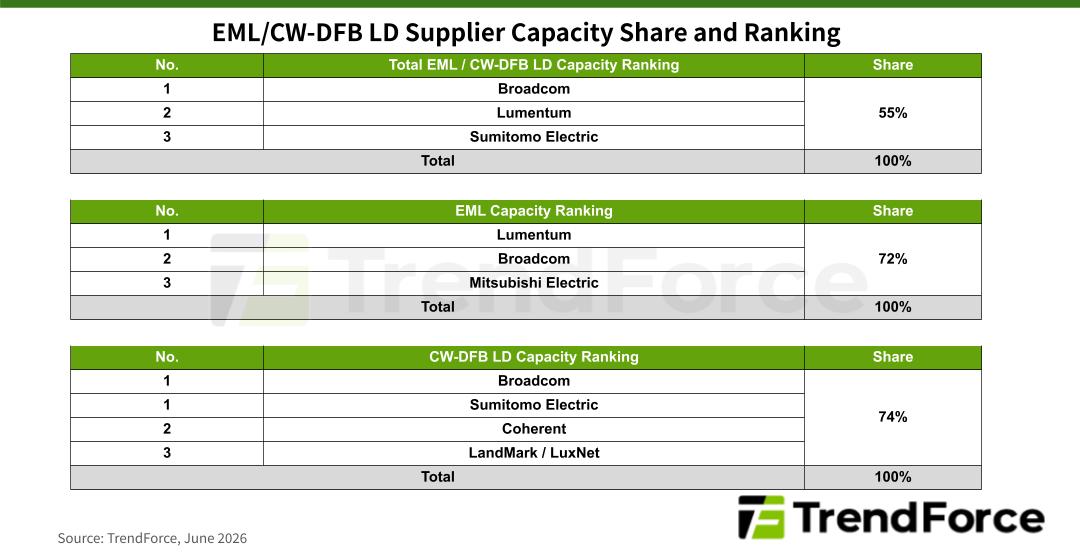

This has prompted suppliers to aggressively expand capacity in response to customer demand, doubling the combined monthly production capacity for EML and CW-DFB LDs to around 50.7 million units in 2026. The top three suppliers, Broadcom, Lumentum, and Sumitomo Electric, are expected to collectively account for 55% of the market.

EMLs are high-performance optical communication components that integrate a laser source and an electro-absorption modulation (EAM) onto a single chip. Since the laser diodes remain continuously active, EMLs offer ultra-low noise interference and extremely narrow spectral characteristics.

This makes them the ideal solution for data transmission exceeding 800 Gbps and for medium-to-long-distance transmission exceeding 2 kilometers. Given the high technical barriers, the top three suppliers—Lumentum, Broadcom, and Mitsubishi Electric—collectively hold approximately 72% market share.

Lumentum is not only aggressively expanding production capacity for 100/200 Gbps EML products, but also successfully demonstrated 400 Gbps-per-lane EML technology at OFC 2026 to address future 3.2 Tbps market demand.

Additionally, while NVIDIA-led EML solutions focus on maximizing signal integrity and transmission performance, other CSPs are actively developing CW-DFB LDs for optical circuit switches (OCS) and silicon photonics co-packaged optics (SiPh CPO) solutions.

Broadcom and Sumitomo Electric currently lead the industry in CW-DFB LD production capacity, followed by Coherent and LandMark/LuxNet. Together, these suppliers account for approximately 74% of total market capacity.

Meanwhile, Coherent is accelerating the transition toward 6-inch InP epi-wafer production to support large-scale manufacturing while also developing 400 mW CW-DFB LDs for silicon photonics pluggable transceivers and co-packaged optics applications.

For more information on TrendForce’s optoelectronics reports and market data, please visit the Report Page, or Email (OR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.