AI Compute Demand Drives 44% YoY Growth for Top 10 Global Fabless IC Firms in 2025, Says TrendForce

Continued investment in AI infrastructure by major CSPs, including purchases of GPUs and deployment of in-house ASICs, has driven strong growth among AI-related chip designers, according to TrendForce’s latest findings.

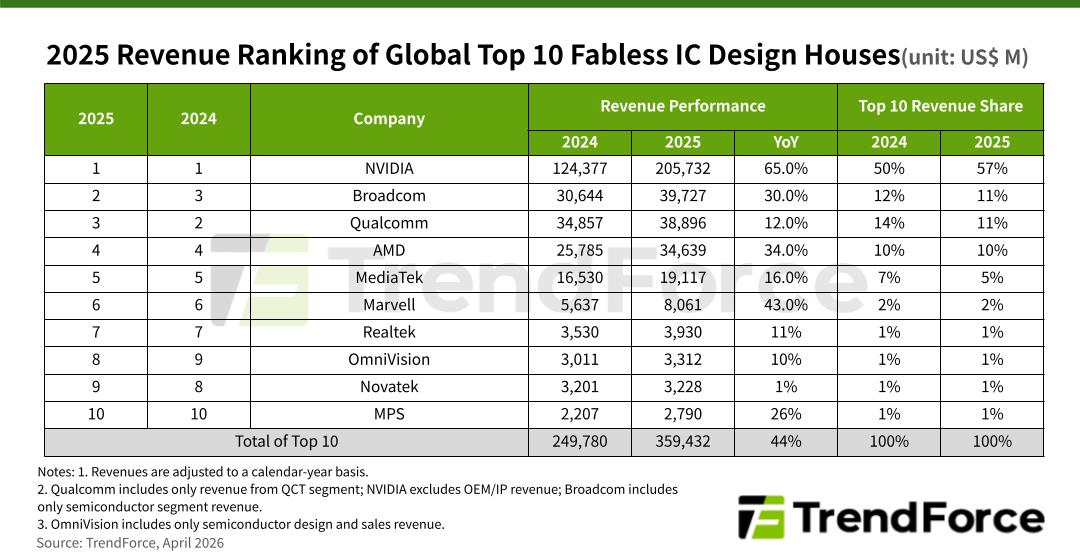

In 2025, the total revenue of the top 10 fabless IC design houses exceeded US$359.4 billion, up 44% YoY. NVIDIA maintained its leading position, while Broadcom moved up to second place due to increased involvement in AI, overtaking Qualcomm, which continues to depend more heavily on consumer electronics.

Industry leader NVIDIA delivered another year of record revenue, supported by its strong AI chip portfolio and computing ecosystem. The company’s fourth quarter revenue from data centers accounted for as much as 90% of its total. Full-year revenue rose 65% YoY to $205.7 billion—the fastest growth among the top players—with its share of total top-ten revenue increasing further to 57%.

Notably, NVIDIA recently announced a $2 billion investment in Marvell. The collaboration will focus on customized XPUs, scale-up interconnect architectures based on NVLink Fusion, as well as optical interconnect and silicon photonics technologies.

Marvell will be able to offer platforms compatible with NVLink Fusion to shared customers, enabling customized ASICs to integrate into NVIDIA’s interconnect ecosystem. This signals that competition in AI infrastructure is expanding beyond the compute performance of GPUs to include interconnect standards and platform integration capabilities.

The AI networking sector is also evolving from a supporting role focused on server connectivity to a critical foundation that determines the efficiency and scalability of AI clusters.

Ranking second, Broadcom benefited from growth in custom silicon and AI networking products, with revenue reaching $39.7 billion in 2025, up 30% YoY. Its performance highlights how the value of AI semiconductors is extending beyond GPUs to customized AI chips and broader network architectures, including Ethernet switches and NICs.

Consumer electronics heavily influenced by economic conditions and replacement cycles; smartphone chips see moderate growth

Chip vendors focused on smartphones are entering a new phase in which growth is driven by premium products but constrained by cost pressures. Qualcomm posted record quarterly growth in 4Q25, driven by shipments of flagship smartphone SoCs. However, given its heavy reliance on mobile, its full-year revenue grew a more modest 12% YoY to nearly $38.9 billion, slipping to third place.

AMD reported over 30% YoY growth in data center revenue in 2025, lifting total revenue by 34% to $34.6 billion and securing fourth place. Its performance reflects the emergence of an alternative supplier alongside NVIDIA in the AI server market, as well as growing demand for open ecosystems.

MediaTek took fifth place, seeing strong shipments of its flagship Dimensity 9500 chipset, which drove full-year revenue to a record $19.1 billion, up 16% YoY.

Marvell ranked sixth, with revenue surpassing $8 billion in 2025, up 43% YoY–second only to NVIDIA in growth. Revenue growth was supported by the rapid adoption of AI data center connectivity, custom silicon, and interconnect technologies.

Realtek’s 4Q25 revenue declined to $847 million due to seasonality and year-end inventory adjustments. However, strong pull-in demand in the first half supported full-year revenue of $3.9 billion, placing it seventh.

OmniVision also saw a quarterly decline in 4Q25, but full-year revenue reached $3.31 billion, moving the company up to eighth place. Growth was driven by increased camera adoption in advanced driver-assistance systems (ADAS) in China, on top of strong demand for action and panoramic cameras boosting its CIS business.

Novatek reported revenue of nearly $3.23 billion in 2025, up 1% YoY, ranking ninth. Quarterly revenue declined in 4Q25 due to seasonal weakness in consumer electronics. Beyond its core driver IC business, the company is expanding into imaging and machine vision SoCs, aiming to increase the share of AI-enabled products.

MPS ranked tenth, with 4Q25 revenue supported by demand for AI and server-related power management solutions. Full-year revenue grew 26% YoY to $2.79 billion. Its strong positioning in data center power management could support further gains in ranking.

For more on the latest technology industry news and trends, please visit News.