Limited Capacity and Order Shifts Drive March Consumer DRAM Price Surge, Led by Sub-4Gb Products, Says TrendForce

Major suppliers are continuing to phase out production of mature products below DDR4, according to TrendForce’s latest research on the memory industry. As supply tightens structurally, DRAM prices have already posted significant cumulative increases in recent months.

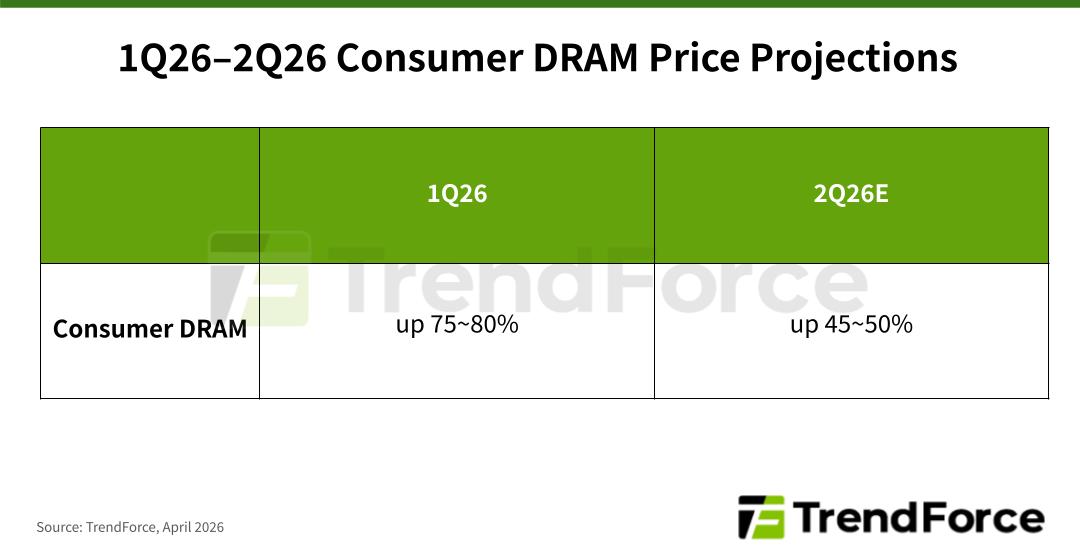

TrendForce forecasts that consumer DRAM contract prices will continue to rise by 45–50% QoQ in 2Q26 after taking into account ongoing supply reductions, order transfers, and the slower pace of capacity expansion among Taiwanese suppliers.

TrendForce reports that in March 2026, the pricing trends in the consumer DRAM sector were mainly driven by products with densities under 4 Gb. For instance, the average prices for DDR4 4 Gb increased by over 20% MoM, far outpacing price increases seen in higher-density products. This followed an earlier price jump in DDR4 and a 2025 announcement from major suppliers that some legacy-node products would be reaching end-of-life (EOL).

Taiwanese manufacturers shifted capacity toward DDR4 to capture the first wave of spillover demand. However, demand is now also shifting into DDR3 and DDR2 markets. With capacity constraints limiting supply, average prices across DDR3 and DDR2 products increased by 20–40% in March, marking an even sharper rise.

Looking ahead to the second quarter, Taiwanese suppliers raised quotations in March, with some prices already reflecting expected second-quarter increases. Furthermore, they’ve adopted a more assertive pricing stance amid constrained capacity and intensifying order migration.

Consequently, transaction price gaps across different customers are expected to narrow significantly in the coming quarter. In contrast, South Korean suppliers already command relatively higher ASPs in the consumer DRAM segment, and are therefore expected to implement more moderate price adjustments in the near term.

For more on the latest technology industry news and trends, please visit News.