Popular Keywords

DRAM

Insights

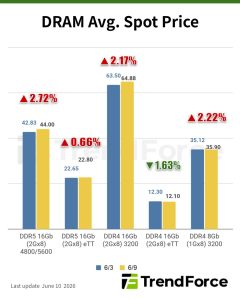

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

News

[News] SK hynix Reportedly to Double DRAM Capacity to 1M Monthly Wafers by 2030, Speeds Yongin Expansion

SK hynix is reportedly preparing a major DRAM capacity expansion. According to The Elec, the company has shared plans with key suppliers to nearly double its DRAM wafer production capacity by 2030–2031 from current levels. The plan aligns with comments made by SK Group Chairman Chey Tae-won at Co...

Insights

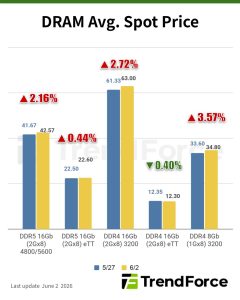

[Insights] Memory Spot Price Update: DDR4 and DDR5 Extend Gains, Though Higher Quotes Temper Procurement Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR4 and DDR5 spot prices continued to rise, with both segments posting notable gains. However, buyers remained cautious amid higher supplier quotes. In the NAND flash segment, spot quotations would continue to slum...

Insights

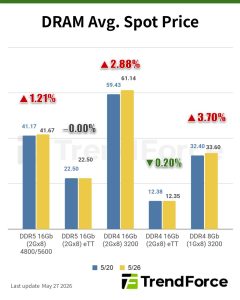

[Insights] Memory Spot Price Update: DDR5 Spot Price Gains Narrow Amid Sluggish Trading; DDR4 Rebounds

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR5 spot price gains narrowed amid sluggish trading, while DDR4 2Gx8-3200 and 1Gx8-3200 prices rebounded after earlier declines. In the NAND flash segment, spot prices are expected to remain under pressure in the n...

Insights

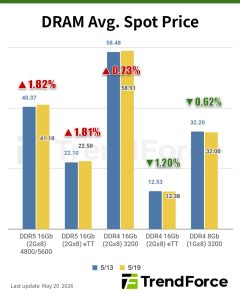

[Insights] Memory Spot Price Update: DDR5 Spots Strengthen on Branded Demand and Higher Bids, DDR4 Weakens

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR5 spot market remained active, with notable inquiries for branded chips, while DDR4 activity stayed subdued. In the NAND flash segment, higher-than-expected 2Q26 contract settlements have provided support to spot...

- Page 2

- 49 page(s)

- 242 result(s)