Popular Keywords

DRAM

Insights

[Insights] Memory Spot Price Update: DRAM Spot Market Strengthens Post-Holiday as DDR4 Leads Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, overall trading conditions improve following holidays in certain regions, with demand concentrated on DRAM suppliers’ DDR4 512x16 and 1Gx16 chips. In the NAND flash segment, the spot market carries on from last we...

Insights

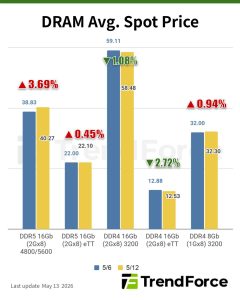

[Insights] Memory Spot Price Update: Buying Interest Stays Focused on DDR5 as Mainstream DDR4 Edges Down 0.25%

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, buying interest remained concentrated on suppliers’ DDR5 chips, while mainstream DDR4 pricing largely moved sideways, with DDR4 1Gx8 3200MT/s chips edging down 0.25% this week. In the NAND flash segment, spot mark...

Insights

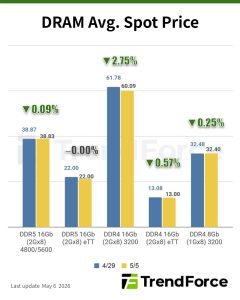

[Insights] Memory Spot Price Update: DDR5 Sees Sporadic Buying Interest; DDR4 Price Cuts Fail to Revive Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, only DDR5 chips saw sporadic buying interest. DDR4 demand remained weak, with price cuts failing to revive purchasing activity. In the NAND flash segment, spot prices continued to drop over the past month, now arriv...

Insights

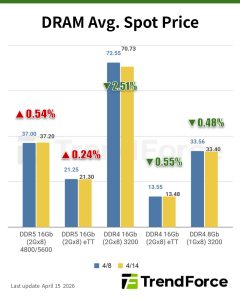

[Insights] Memory Spot Price Update: DRAM Spot Sellers Hold Firm Ahead of Mid-April Pricing, DDR4 Edges Lower 0.48%

According to TrendForce’s latest memory spot price trend report, in the DRAM segment, most spot sellers held firm on quoted prices ahead of mid-April official pricing announcements. However, weak end-demand and cautious purchasing behavior kept overall trading activity subdued. As a result, the av...

Insights

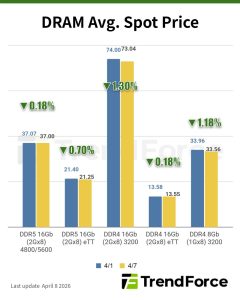

[Insights] Memory Spot Price Update: DRAM Extends Gradual Downtrend on Contained Selling Pressure; DDR4 Drops 1.18%

According to TrendForce's latest memory spot price trend report, DRAM continues to face contained selling pressure, with spot prices maintaining a gradual downward trend. In the NAND segment, most sellers are expecting further increases in 2Q26 contract prices, in an attempt to lift spot prices as w...

- Page 3

- 49 page(s)

- 242 result(s)