Popular Keywords

DRAM

Insights

[Insights] Memory Spot Price Update: DRAM Spot Prices See Gains in Low-Density DDR4 and DDR3 Amid Sideways Market

According to TrendForce’s latest memory spot price trend report, DRAM spot prices this week have seen upward momentum in low-density DDR4 and DDR3 segments, while the broader market continues to trend sideways. In NAND Flash, suppliers are adjusting quotations to optimize inventory levels, but buy...

Insights

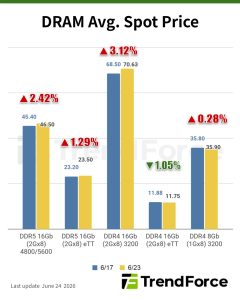

[Insights] Memory Spot Price Update: DRAM Buyers Resist Higher Quotes as Mainstream DDR4 Prices Gain 0.28%

According to TrendForce’s latest memory spot price trend report, DRAM trading remained subdued as buyers showed little willingness to follow higher quotations, with mainstream DDR4 chips (DDR4 1Gx8 3200MT/s) edging up 0.28% this week. In NAND flash, diverging expectations between buyers and seller...

Insights

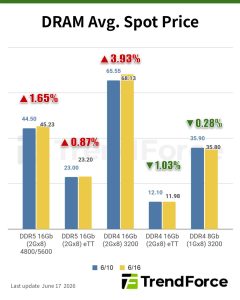

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

News

[News] Huawei, Xiaomi Reportedly Plan HBM-Inspired LLW DRAM for 2H27 to Boost On-Device AI in Smartphones

While smartphone form factors and thermal constraints have limited HBM adoption, Chinese smartphone brands are reportedly exploring HBM-inspired memory architectures. According to Wccftech, citing Weibo tipster Fixed-focus Digital, Xiaomi and Huawei may be planning to introduce custom Low Latency Wi...

News

[News] South Korea Chip Export Volume Falls Yet Revenue Surges; May DRAM +370%, NAND +207%

Rising memory prices are creating an unusual divergence in South Korea's semiconductor export data. As noted by Seoul Economic Daily, export revenue is rising sharply even as export volume by weight declines, highlighting growing demand for lightweight, high-value chips such as HBM. As the report...

- Page 1

- 49 page(s)

- 242 result(s)