Popular Keywords

DRAM

Insights

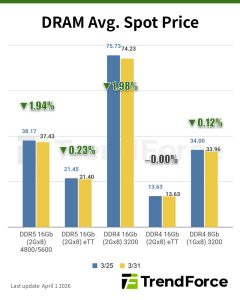

[Insights] Memory Spot Price Update: DDR3 Strength Contrasts Weak DDR4/ DDR5 Amid High Prices, Soft Demand

According to TrendForce's latest memory spot price trend report, regarding DRAM, momentum in both DDR4 and DDR5 remains weak, as end-user demand continues to struggle with elevated price levels, while 2Q26 contract pricing has yet to be formally announced. Meanwhile, in terms of NAND, module houses ...

Insights

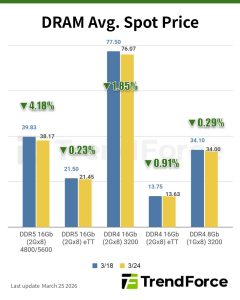

[Insights] Memory Spot Price Update: DRAM Spot Momentum Constrained as March Contracts Hold, DDR4 Weakest

According to TrendForce's latest memory spot price trend report, regarding DRAM, upward momentum in the DRAM spot market has been constrained, with the DDR4 segment being particularly weak. Meanwhile, in terms of NAND, as negotiations for contract prices of the new quarter gradually approach, the sp...

Insights

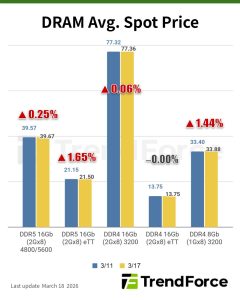

[Insights] Memory Spot Price Update: DRAM Spots Pause Amid Samsung’s March DDR4 Freeze

According to TrendForce's latest memory spot price trend report, regarding DRAM, with Samsung pausing DDR4 consumer chip price hikes in March, increases are expected to stall briefly before picking up again in 2Q26. Meanwhile, in terms of NAND, with the expectation on significant increases on contra...

News

[News] Nanya Tech: DRAM Up Month by Month in 1Q, Sharp 2Q Jump Ahead, Shortage Through 2028

As memory prices accelerate on tight supply, major vendors led by Samsung have launched fresh DRAM hikes. Against this backdrop, Taiwan’s top DRAM maker Nanya Technology said prices are still rising month by month this quarter, with second-quarter quotes poised to “jump” sharply, according to ...

Insights

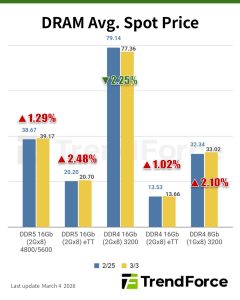

[Insights] Memory Spot Price Update: DRAM Spots Top Contracts, Sentiment Cautious Ahead of Q2 Negotiations

According to TrendForce's latest memory spot price trend report, regarding DRAM, as current spot prices remain higher than contract prices, and negotiations for 2Q26 pricing have not yet started, an overall wait-and-see atmosphere prevails. Meanwhile, NAND spot prices maintain an upward trend, climb...

- Page 4

- 49 page(s)

- 242 result(s)