Popular Keywords

DRAM

News

[News] Decoding Micron’s SCAs: Reportedly 20% of DRAM Output, Toward 50% of Long-Term Memory Revenue

Shortly after announcing a strategic agreement with Anthropic covering AI memory and storage architecture design—part of its broader push into Strategic Customer Agreements (SCAs)—Micron expanded on its long-term deal pipeline during its latest earnings call. According to Investing.com, the c...

News

[News] Micron Profit Surges 15-Fold as Margin Nears 85%; HBM4 Revenue Exceeds $1B

Fueled by the AI boom, Micron delivered another blockbuster quarter in 3QFY2026, with revenue surging 74% sequentially and profit more than doubling from the previous quarter, according to its press release. Gross margin climbed to a record 84.9%, well above the company's 81% forecast and up sharply...

Insights

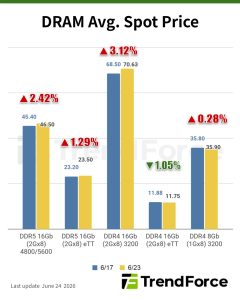

[Insights] Memory Spot Price Update: DRAM Buyers Resist Higher Quotes as Mainstream DDR4 Prices Gain 0.28%

According to TrendForce’s latest memory spot price trend report, DRAM trading remained subdued as buyers showed little willingness to follow higher quotations, with mainstream DDR4 chips (DDR4 1Gx8 3200MT/s) edging up 0.28% this week. In NAND flash, diverging expectations between buyers and seller...

News

[News] Memory Giants Split on HBM4 Strategy: Samsung HBM4 Sales Reportedly Tops $1B, SK hynix Slows Ramp

As memory giants accelerate their next-generation HBM race, Samsung Electronics has reportedly hit a key milestone. According to Yonhap News and ZDNet, its HBM4 has surpassed US$1 billion in revenue, making it the first product in the industry to reach the level just four months after entering mass ...

News

[News] SK hynix Reported Design Hiring Surge Tightens Chip Talent Market, Raises Samsung Concerns

As next-gen memory tech like HBM, SOCAMM, and 3D NAND increasingly need stronger chip design and advanced packaging capabilities, SK hynix, according to The Elec, has launched an unusually large-scale recruitment of design engineers. According to the report, the memory giant plans to hire a tripl...

- Page 2

- 144 page(s)

- 716 result(s)