Popular Keywords

DRAM

News

[News] SK Hynix Commits Additional USD 15 Billion, Escalating Fab Expansion Race among Memory Giants

On February 25, global memory leader SK hynix announced that its board of directors has approved an additional investment of approx. KRW 21.6 trillion (~ USD 15 billion) for its first semiconductor fabrication plant by the end of December 2030. The funds will be used to finalize construction of t...

Insights

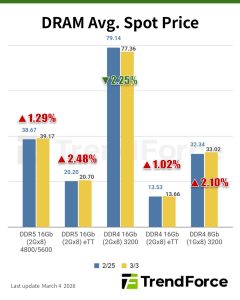

[Insights] Memory Spot Price Update: DRAM Spots Top Contracts, Sentiment Cautious Ahead of Q2 Negotiations

According to TrendForce's latest memory spot price trend report, regarding DRAM, as current spot prices remain higher than contract prices, and negotiations for 2Q26 pricing have not yet started, an overall wait-and-see atmosphere prevails. Meanwhile, NAND spot prices maintain an upward trend, climb...

News

[News] Asia’s Chipmakers Reportedly Eye $136B Spend in 2026, Up 25% YoY, Spanning Foundry and Memory

Fueled by soaring demand for AI chips, memory, and logic processors, Asia’s top chipmakers are ramping up their 2026 capital spending. Nikkei and TrendForce report that leading semiconductor firms across South Korea, Taiwan, Japan, and China plan to invest over $136 billion this year, a 25% increa...

News

[News] SOCAMM War Heats up: Micron Ships 256GB SOCAMM2 Samples, Topping Industry Capacity

Shortly after confirming that it had begun sampling its 192GB SOCAMM2 last October, Micron has moved a step further. According to a new press release, the company has started shipping customer samples of a 256GB SOCAMM2 — currently the highest-capacity LPDRAM module in the industry. Micron said...

News

[News] Inside Look at Micron’s Newly Opened Sanand Plant: 10% of Global Output, Key Products and Clients

With the launch of Micron’s semiconductor assembly and test facility in Sanand, Gujarat on February 28, India has formally stepped onto the global memory map. Below are key highlights of the new plant, its role in Micron’s worldwide operations, and why it represents a pivotal milestone in India�...

- Page 22

- 144 page(s)

- 719 result(s)