Popular Keywords

DRAM

News

[News] Micron Taps Bechtel, Intel Ohio Fab Builder, to Speed Up New York Mega Fab Construction

Micron, which broke ground on its New York mega fab in January, has now moved to accelerate the project by naming its lead contractor. According to syracuse.com, engineering and construction giant Bechtel—also in charge of Intel’s Ohio semiconductor campus—will handle the engineering, procurem...

News

[News] SK hynix Advances DRAM and NAND Roadmap, Targets 3x Wafer Output by 2034, 375-Layer NAND at Year-End

While SK hynix had only last week outlined plans to double capacity over the next five years, the memory giant is now signaling an even more aggressive expansion across both DRAM and NAND. According to Nikkei, citing Chairman Chey Tae-won, the company is targeting a threefold increase in wafer outpu...

News

[News] Lenovo Reportedly Set for July Price Hikes Across Product Portfolio as Memory Costs Pressure PC Market

With memory prices remaining elevated, consumer electronics could be heading for another round of price increases. Chinese media outlet Lanjinger.com, citing sources familiar with the matter, reports that Lenovo plans to raise prices across its product lineup from July, broadly in line with the prev...

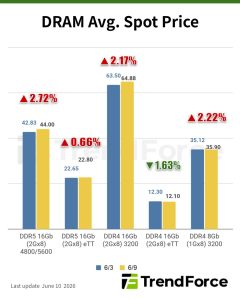

Insights

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

News

[News] SK hynix Reportedly Places 44.2bn Won TC Bonder Order with Hanmi, Accelerating HBM4 Ramp-up

Following Jensen Huang’s push for higher HBM supply from SK hynix, the memory maker has taken another step to ramp up production. According to ET News, SK hynix has placed a 44.2 billion won order with Hanmi Semiconductor for TC (thermal compression) bonders used in sixth-generation HBM (HBM4) pro...

- Page 4

- 144 page(s)

- 716 result(s)