SpaceX IPO Momentum to Drive Global Satellite Industry Output Value to $447 Billion by 2027, as Taiwanese Firms Target Satellite Communications and AI Space Computing Opportunities, Says TrendForce

SpaceX’s upcoming IPO plans have become a significant market focus, driven by rising global demand for satellite broadband, direct-to-cell (DTC) connectivity, and AI computing. According to TrendForce, SpaceX is expanding its satellite broadband coverage and aggressively entering new sectors such as DTC services, AI space computing, and space-based solar power (SBSP).

By developing its own AI space computing chip facility, Terafab, SpaceX is enhancing its vertical integration and shifting the LEO satellite industry from a purely communication service to a new era of computing services. The global space economy is entering a growth phase as satellite networks, AI infrastructure, and space applications increasingly integrate. TrendForce predicts that the worldwide satellite industry will generate $447 billion by 2027, with an annual growth rate of 14%.

TrendForce notes that following SpaceX’s large-scale acquisition of EchoStar’s AWS-3, AWS-4, and H-Block spectrum assets, the company is expected to accelerate deployment of DTC satellite services in emerging markets as it expands its LEO communications footprint.

SpaceX is enhancing AI space computing by analyzing agricultural monitoring, maritime tracking, and environmental surveillance images directly in orbit, then transmitting only the processed results to ground networks. This method reduces requirements for data transmission and the AI processing load on terrestrial data centers.

Additionally, SpaceX is gradually building a comprehensive LEO system spanning terrestrial and orbital infrastructure by integrating satellite communications, reusable rockets, and AI computing platforms—strengthening its competitive position in the global satellite communications and space computing markets.

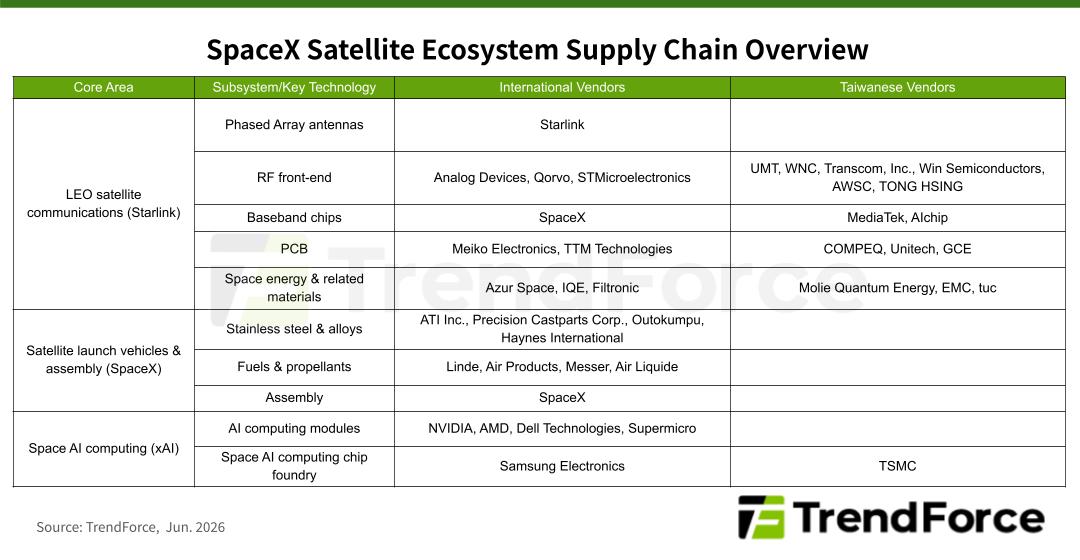

Starlink’s supply chain includes key components such as satellite antenna modules, RF front-end modules, PCBs, and beamforming ICs. SpaceX has been developing its own beamforming ICs internally, while STMicroelectronics supplies antenna RF chips. Germany-based Azur Space provides solar cells for Starshield, while UK firms IQE and Filtronic supply compound semiconductor materials such as GaAs and GaN.

Through its combination of proprietary chip development and international supply chain partnerships, SpaceX continues improving satellite communication performance and deployment scale, while simultaneously driving demand growth for high-frequency communications, advanced semiconductors, and aerospace components.

In rocket and satellite manufacturing, suppliers including ATI and Precision Castparts (PCC) provide high-temperature alloys, titanium alloys, and precision cast components used in the Raptor engine and Starship platform. Industrial gas providers such as Linde and Air Products supply cryogenic gases including liquid oxygen (LOX) and liquid nitrogen (LN2) to support rocket testing, launch operations, and ground infrastructure.

In the realm of AI space computing, NVIDIA has introduced the Space-1 Vera Rubin in-orbit AI computing platform, while AMD is expanding into radiation-hardened FPGA and high-performance computing (HPC) solutions through products such as the Kintex UltraScale XQR FGPAs to support future autonomous satellite computing requirements.

Meanwhile, SpaceX’s xAI is rapidly advancing AI-powered in-orbit satellite development, with Samsung Electronics and TSMC reportedly involved in early-stage small-volume production of AI space computing chips.

Taiwanese suppliers are increasingly entering key segments of the space supply chain through strengths in precision manufacturing and non-China supply chain positioning as SpaceX accelerates expansion in satellite communications and AI space computing.

Among Taiwanese companies, UMT supplies high-frequency microwave components and filters. COMPEQ is benefiting from expanding Starlink satellite deployments and rising demand for in-orbit AI computing, increasing shipments of high-end HDI boards while also developing dedicated high-frequency HDI boards for AI computing.

In satellite terminal equipment, WNC has entered the Starlink supply chain through its antenna design and RF system integration capabilities.

TSEC Corp and Molie Quantum Energy supply solar cells and high-power lithium batteries, respectively, while EMC and ITEQ provide high-end copper clad laminate (CCL). TSMC is expected to continue securing manufacturing orders for AI space computing chips.

TrendForce believes that as satellite communications and AI computing continue converging, Taiwanese suppliers will play an increasingly important role within the global space industry supply chain.

For more information on reports and market data from TrendForce’s Department of ICT Applications Research, please Email (TRI_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.