Global Direct-to-Cell Market to Grow 49% YoY in 2026, Unlocking New Supply Chain Opportunities, Says TrendForce

Direct-to-Cell technology is rapidly maturing as global mobile communications standards 3GPP Release 17 and Release 18 continue to incorporate satellite communications. TrendForce’s findings indicate that satellite operators are shifting from traditional satellite broadband services to direct satellite connectivity for smartphones. The global market is projected to reach US$7.6 billion in 2026, representing approximately 49% YoY growth.

TrendForce notes that Direct-to-Cell technology effectively addresses connectivity gaps in remote areas without terrestrial base stations and significantly improves the efficiency of emergency communication.

Starlink officially launched its Starlink Mobile service at MWC 2026. It boasts greatly enhanced signal reliability, thanks to its fleet of next-generation V2 satellites in low Earth orbit, expanding services from text messaging to voice and video transmission. Meanwhile, AST SpaceMobile is expected to roll out full-service offerings, including messaging, voice, and video, in the U.S. and Japan in 2026.

Direct-to-Cell adoption is rapidly increasing, supported by major telecom operators, with growth in both user numbers and engagement. The user base is broadening from individual consumers to include enterprise clients. For instance, mining firms and large agricultural companies in remote U.S. areas are eager to subscribe because they need real-time data in locations with poor connectivity. Consequently, both Starlink and AST SpaceMobile are focusing on the U.S. market to quickly build commercial momentum.

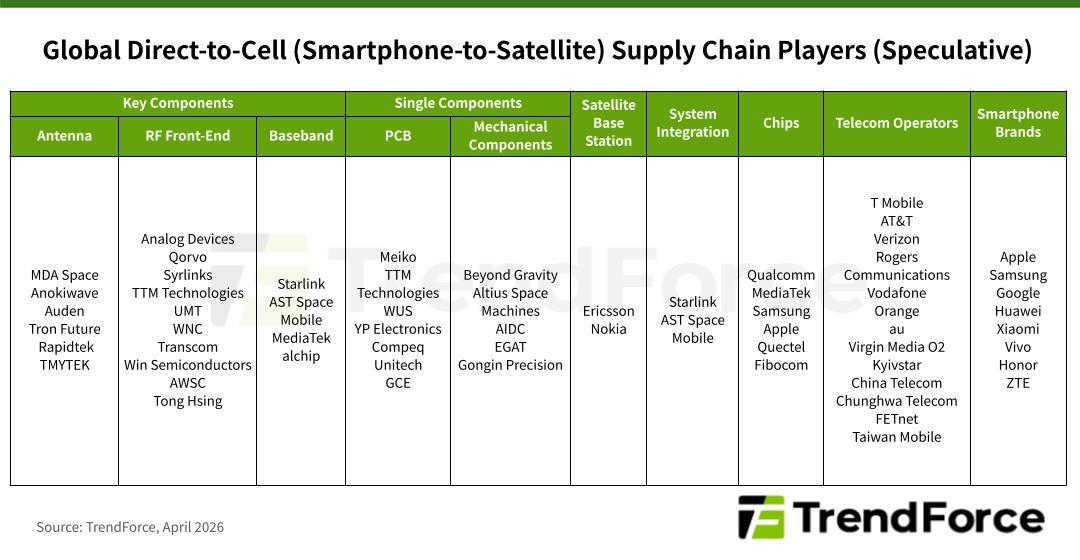

Breaking down the supply chain, the upstream segment focuses on key components, including antennas, RF front-end modules, and baseband chips. Companies such as Analog Devices and Qorvo supply RF modules, while satellite operators like Starlink and AST SpaceMobile have developed baseband solutions to address high-latency challenges in space communications.

The midstream focuses on satellite-based base stations and system integration, where component suppliers provide modules that are then integrated into complete satellite systems by operators such as Starlink and AST SpaceMobile. Downstream includes smartphone brands and telecom operators, with manufacturers such as Samsung, Google, and Vivo adopting satellite communication chips from Qualcomm and MediaTek, and telecom providers offering corresponding services.

Taiwan’s communications component industry already demonstrates strong capabilities across the value chain, from key components to subsystem integration, including Ka-band phased array antennas, GaN high-power chips, and RF module integration.

This positions Taiwanese companies well to enter the supply chains of major players like Starlink and AST Spacemobile. However, challenges remain in high-barrier technologies such as inter-satellite laser communication (ISL), where limitations in system integration capabilities persist.

For more on the latest technology industry news and trends, please visit News.