Popular Keywords

DDR4

Insights

[Insights] Memory Spot Price Update: DRAM Spot Prices See Gains in Low-Density DDR4 and DDR3 Amid Sideways Market

According to TrendForce’s latest memory spot price trend report, DRAM spot prices this week have seen upward momentum in low-density DDR4 and DDR3 segments, while the broader market continues to trend sideways. In NAND Flash, suppliers are adjusting quotations to optimize inventory levels, but buy...

Insights

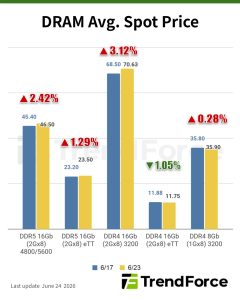

[Insights] Memory Spot Price Update: DRAM Buyers Resist Higher Quotes as Mainstream DDR4 Prices Gain 0.28%

According to TrendForce’s latest memory spot price trend report, DRAM trading remained subdued as buyers showed little willingness to follow higher quotations, with mainstream DDR4 chips (DDR4 1Gx8 3200MT/s) edging up 0.28% this week. In NAND flash, diverging expectations between buyers and seller...

Insights

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

Insights

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

News

[News] Motherboard and Module Makers Reportedly Expand DDR4 Platforms Amid Rising DDR5 Costs

Several vendors are reportedly ramping up DDR4 production as demand remains strong. According to Wccftech, higher DDR5 prices are contributing to stronger demand for DDR4 platforms. While DDR4 prices have also increased, they remain significantly lower than those of comparable DDR5 modules. The repo...

- Page 1

- 15 page(s)

- 73 result(s)