Popular Keywords

DDR4

Insights

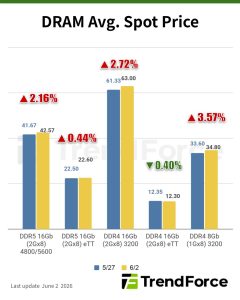

[Insights] Memory Spot Price Update: DDR4 and DDR5 Extend Gains, Though Higher Quotes Temper Procurement Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR4 and DDR5 spot prices continued to rise, with both segments posting notable gains. However, buyers remained cautious amid higher supplier quotes. In the NAND flash segment, spot quotations would continue to slum...

Insights

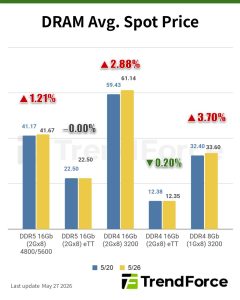

[Insights] Memory Spot Price Update: DDR5 Spot Price Gains Narrow Amid Sluggish Trading; DDR4 Rebounds

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR5 spot price gains narrowed amid sluggish trading, while DDR4 2Gx8-3200 and 1Gx8-3200 prices rebounded after earlier declines. In the NAND flash segment, spot prices are expected to remain under pressure in the n...

News

[News] DDR4 Shortage Reportedly Limits Nanya Tech’s DDR5 Shift; GM Says DRAM Margins Across Segments Top HBM

As global memory giants led by Samsung phase out DDR4 production, Taiwanese DRAM maker Nanya Technology is emerging as a key beneficiary of the resulting supply squeeze. According to Yahoo! Finance, General Manager Lee Pei-ying said that due to a significant supply gap in DDR4 and LPDDR4, many custo...

Insights

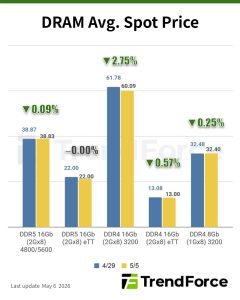

[Insights] Memory Spot Price Update: Buying Interest Stays Focused on DDR5 as Mainstream DDR4 Edges Down 0.25%

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, buying interest remained concentrated on suppliers’ DDR5 chips, while mainstream DDR4 pricing largely moved sideways, with DDR4 1Gx8 3200MT/s chips edging down 0.25% this week. In the NAND flash segment, spot mark...

Insights

[Insights] Memory Spot Price Update: DDR5 Sees Sporadic Buying Interest; DDR4 Price Cuts Fail to Revive Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, only DDR5 chips saw sporadic buying interest. DDR4 demand remained weak, with price cuts failing to revive purchasing activity. In the NAND flash segment, spot prices continued to drop over the past month, now arriv...

- Page 2

- 15 page(s)

- 73 result(s)