Popular Keywords

NAND Flash

Insights

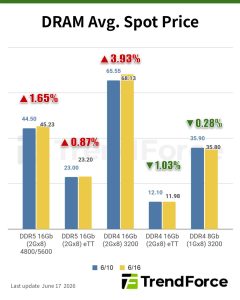

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

News

[News] Key Semiconductor Gas WF₆ Prices Reportedly Surge Over 200% as Supply Tightens Ahead of Japan Output Cuts

While China’s rare earth export controls continue to draw market attention, another key semiconductor material is also seeing sharp price swings. According to chinastarmarket.cn, citing China’s General Administration of Customs, tungsten hexafluoride (WF₆) hit $149.79 per kilogram in April 202...

News

[News] The Race to 400-Layer NAND: Roadmaps and Key Technologies Driving Samsung, SK hynix, and Kioxia

As SK hynix reportedly targets mass production of 375-layer NAND by year-end, according to The Elec, the 400-layer threshold is increasingly seen as a key technical frontier in advanced NAND scaling. Against this backdrop, ET News notes that Samsung began mass producing its 286-layer NAND in Apri...

News

[News] SK hynix Advances DRAM and NAND Roadmap, Targets 3x Wafer Output by 2034, 375-Layer NAND at Year-End

While SK hynix had only last week outlined plans to double capacity over the next five years, the memory giant is now signaling an even more aggressive expansion across both DRAM and NAND. According to Nikkei, citing Chairman Chey Tae-won, the company is targeting a threefold increase in wafer outpu...

Insights

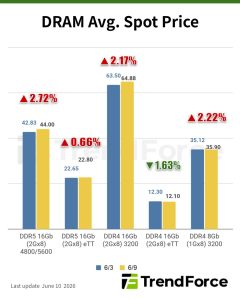

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

- Page 4

- 81 page(s)

- 404 result(s)