Popular Keywords

NAND Flash

News

[News] Decoding Micron’s SCAs: Reportedly 20% of DRAM Output, Toward 50% of Long-Term Memory Revenue

Shortly after announcing a strategic agreement with Anthropic covering AI memory and storage architecture design—part of its broader push into Strategic Customer Agreements (SCAs)—Micron expanded on its long-term deal pipeline during its latest earnings call. According to Investing.com, the c...

News

[News] Micron Profit Surges 15-Fold as Margin Nears 85%; HBM4 Revenue Exceeds $1B

Fueled by the AI boom, Micron delivered another blockbuster quarter in 3QFY2026, with revenue surging 74% sequentially and profit more than doubling from the previous quarter, according to its press release. Gross margin climbed to a record 84.9%, well above the company's 81% forecast and up sharply...

News

[News] Kioxia Executive Pay Reportedly Surges Multiple-Fold, Converging toward Samsung and SK hynix Peer Levels

As Kioxia’s market capitalization briefly surpassed Toyota Motor in June to become Japan’s largest listed company, attention is also turning to the company’s top executive compensation. According to Bloomberg, citing Kioxia’s freshly revealed securities report (year ended March 2026), Execut...

Insights

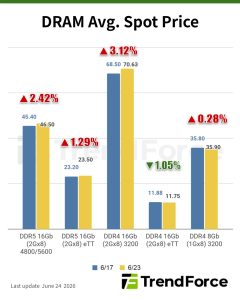

[Insights] Memory Spot Price Update: DRAM Buyers Resist Higher Quotes as Mainstream DDR4 Prices Gain 0.28%

According to TrendForce’s latest memory spot price trend report, DRAM trading remained subdued as buyers showed little willingness to follow higher quotations, with mainstream DDR4 chips (DDR4 1Gx8 3200MT/s) edging up 0.28% this week. In NAND flash, diverging expectations between buyers and seller...

News

[News] Samsung Unveils UFS 5.0 Storage, Claims Industry’s Fastest with 10.8GB/s Speeds

While advancing its next-generation HBM development, Samsung is also pushing forward on the NAND front, unveiling what it claims is the industry’s first and fastest Universal Flash Storage (UFS) 5.0 solution. According to Samsung, the device delivers sequential read speeds of up to 10.8 GB/s and w...

- Page 2

- 81 page(s)

- 402 result(s)