Popular Keywords

NAND Flash

News

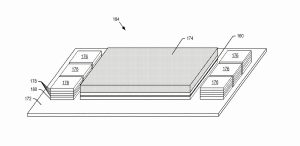

[News] SanDisk Goes Beyond HBF: Patent Bonds Processor onto NAND Tile, with HBM Stacks on Shared Interposer

While SanDisk is speeding up the development of High Bandwidth Flash (HBF), a next-generation architecture that vertically stacks NAND, the company is also advancing additional memory concepts aimed at addressing structural capacity constraints. According to a U.S. patent (US 12,430,274 B2) filed...

News

[News] Micron Earnings Preview: Four Key Areas in Focus — HBM Progress, Capex and More

As Micron prepares to report its fiscal third-quarter results on June 24, investor attention is turning to whether its strong earnings and elevated margins can be sustained, and how long the ongoing memory rally can support its growth story in DRAM and HBM. Here are four key areas to watch in the up...

News

[News] Kioxia Adopts Cautious Capex Despite NAND Upcycle: Reportedly 10% Below FY23 Peak, Key Concerns in Focus

As Kioxia briefly saw its market capitalization exceed ¥50 trillion on June 16—becoming only the second Japanese firm to reach that level—focus has turned to whether the NAND upcycle can sustain its momentum. Notably, Global Economic News, citing Nikkei, reports that the company is taking a mor...

Insights

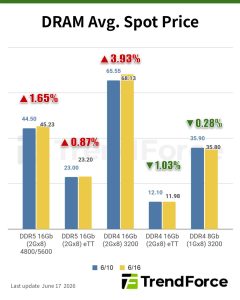

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

News

[News] Key Semiconductor Gas WF₆ Prices Reportedly Surge Over 200% as Supply Tightens Ahead of Japan Output Cuts

While China’s rare earth export controls continue to draw market attention, another key semiconductor material is also seeing sharp price swings. According to chinastarmarket.cn, citing China’s General Administration of Customs, tungsten hexafluoride (WF₆) hit $149.79 per kilogram in April 202...

- Page 3

- 81 page(s)

- 402 result(s)