Contract Prices Surged More Than 100% in 1H26; Structural Shortages to Keep NOR Flash and SLC NAND Prices Rising in 2H26, Says TrendForce

Major memory suppliers continue to prioritize capacity allocation toward higher-value products such as HBM and advanced-layer 3D NAND, according to TrendForce’s latest research on the memory industry. This has squeezed the mature-node capacity for NOR Flash and SLC NAND.

Against a backdrop of steady demand, cumulative contract price increases for both product categories exceeded 100% during the first half of 2026. TrendForce expects prices for NOR Flash and SLC NAND to continue rising in the second half of the year, given that no significant capacity expansion plans have been announced by suppliers, amid tight supply-demand conditions.

TrendForce notes that the core value of NOR Flash lies in its execute-in-place (XIP) capability and high reliability. Firmware requirements in automotive electronics are expanding rapidly as advanced driver-assistance (ADAS) and smart cockpit functions become more sophisticated, making high-density NOR Flash an increasingly critical component.

In edge AI devices, firmware capacities that previously required only tens of megabytes are now growing multiple times larger due to the localized deployment of AI models. This is driving strong demand for high-density NOR Flash solutions of 256 Mb and above. In industrial control systems, satellite communications, and aerospace equipment, NOR Flash remains difficult to replace due to its reliability advantages, creating a stable and high-margin demand base.

SLC NAND, meanwhile, remains the preferred storage technology for many high-reliability applications thanks to its superior program/erase endurance, extremely low error rates, long-term data retention, and wide operating temperature range. The increasing adoption of inference AI in smart factories, robotics, autonomous mobile equipment, and high-end networking switches has further strengthened demand for highly reliable storage solutions.

Enterprise servers and data centers continue to utilize SLC NAND for operating system boot drives and write-intensive buffer applications. In medical imaging equipment, defense electronics, and aerospace systems—where data integrity is mission-critical—SLC NAND retains an irreplaceable position.

TrendForce observes that memory demand gradually recovered during the first half of 2026, while rapid growth in AI-related applications consumed much of the market’s limited supply. NOR Flash was among the first products to experience extended lead times and allocation measures. Average contract prices are estimated to have increased by 100–120% during 1H26, with higher-capacity products seeing even stronger gains.

SLC NAND supply contracted significantly as several international vendors gradually exited low-capacity and mature-node product segments. At the same time, industrial, automotive, and networking customers began rebuilding strategic inventories, triggering a pronounced wave of precautionary purchasing in the second quarter. Average SLC NAND prices surged by an estimated 130–150% during the first half of the year.

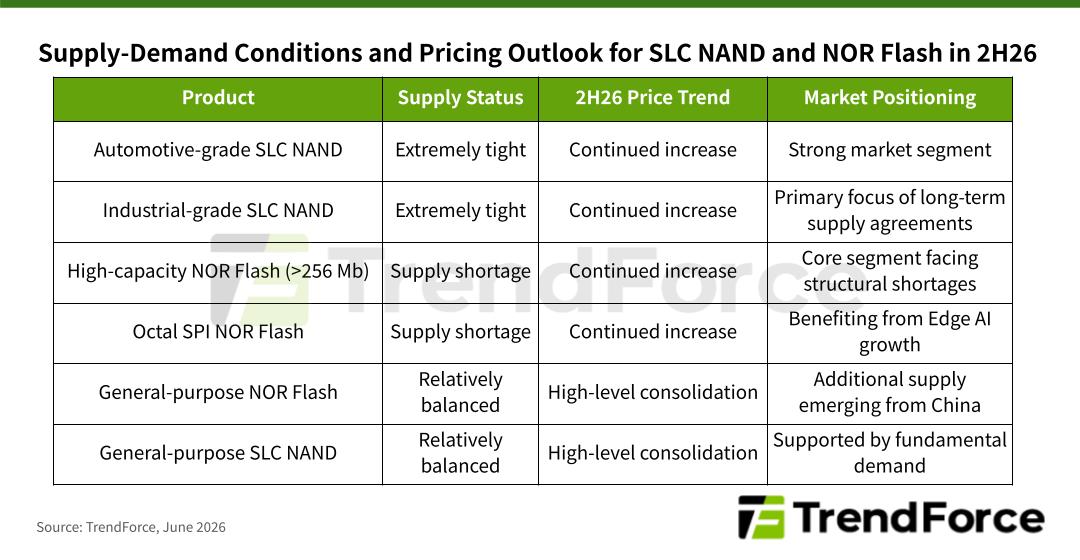

Looking ahead to 2H26, major suppliers will remain focused on process migration, yield improvements, and wafer output optimization rather than capacity expansion. As a result, TrendForce expects long-lifecycle automotive and industrial applications to face an elevated risk of prolonged shortages.

High-density NOR Flash products are expected to benefit from continued growth in demand for automotive electronics and edge AI applications, with prices potentially rising by another 60–65% or more in the second half of the year. By contrast, price increases for lower-density NOR Flash products may moderate as additional capacity from Chinese suppliers gradually enters the market, with some segments potentially entering a period of price stabilization.

Although demand growth for most SLC NAND products remains relatively modest, supply availability continues to decline. TrendForce therefore forecasts that SLC NAND prices will continue to rise in 2H26, albeit at a slower pace than in the first half, with average increases of 70–75% still possible. Industrial-grade and automotive-grade products may experience even stronger price momentum.

TrendForce adds that major suppliers are increasingly likely to manage supply and demand through long-term agreements (LTAs) and selective order acceptance strategies, rather than relying solely on aggressive price increases. This reflects a broader shift in market competition, where supply assurance and customer relationship management are becoming as important as pricing itself.

For more on the latest technology industry news and trends, please visit News.