Global EV Traction Inverter Installations Reach New High in 4Q25; High-Voltage Platform Adoption Continues to Rise, Says TrendForce

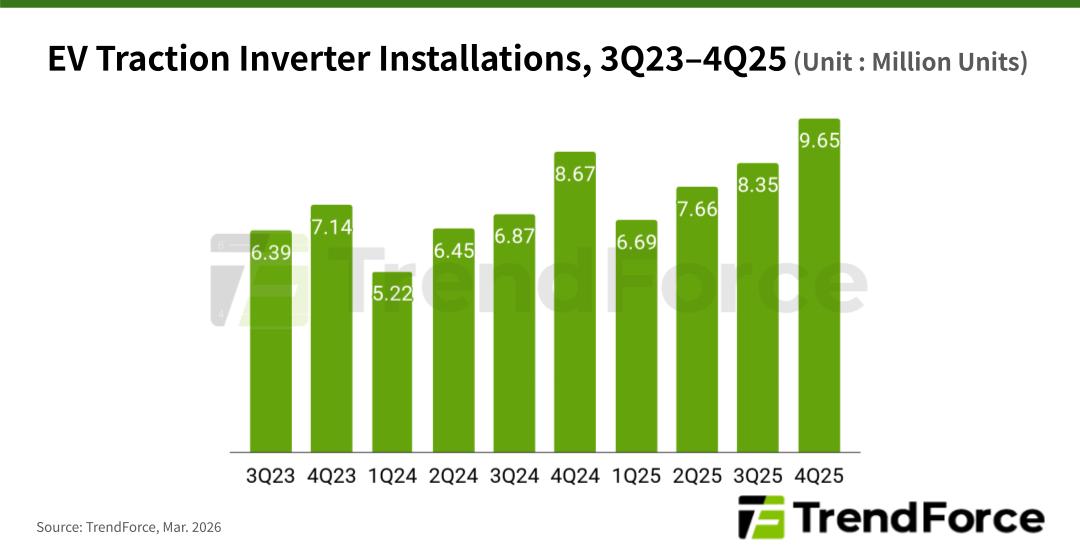

TrendForce’s latest research on EV traction inverters reveals that strong growth in BEV sales in 4Q25 drove global traction inverter installations to around 9.65 million units, marking the highest level in nearly two years. The result reflects the continued shift toward vehicle electrification and the increasing adoption of electric drive systems per vehicle.

Looking at quarterly trends, inverter shipments already surpassed 8.67 million units in 4Q24, supported by the seasonal peak in vehicle sales. In 4Q25, demand in both China and Europe recovered, pushing shipments even higher.

Although declining component costs caused total market revenue to edge down from US$5.5 billion to $5.3 billion, the market continued to demonstrate a pattern of rising volumes with relatively stable pricing. This suggests that ongoing technological upgrades are helping maintain ASPs despite intensifying competition.

High-voltage systems above 550V—typically associated with 800V architectures—recorded the fastest growth in 4Q25, with installations rising 38% YoY to approximately 1.39 million units. Their market penetration increased to 14%.

Systems operating in the 300V to 550V range remain the dominant segment, with installations reaching 6.04 million units. In contrast, systems below 300V declined 11% compared with the same period in 2024. The shift toward higher-voltage platforms is accelerating the adoption of SiC power devices, which improve electric drive efficiency and enable faster charging.

Overall market concentration remains relatively stable. BYD continues to lead the market, holding roughly 17% share in 4Q25 as the company benefits significantly from its vertically integrated business model.

Denso accounted for about 11% of the market, maintaining its position as a core supplier within the Japanese automotive supply chain.

Other Chinese suppliers, including Huawei and Inovance, each held around 4–5% market share. Together with BYD’s leadership, these figures highlight the growing momentum behind China’s localization of electrical driving technologies.

TrendForce notes that the global traction inverter market is transitioning from an early stage of rapid expansion to a phase defined by scale and technological advancement.

Future growth will be driven by several factors, including the wider adoption of 800V high-voltage platforms, the increasing use of integrated multi-in-one electric drive systems, and the declining cost of SiC power modules.

As automakers strengthen their in-house development capabilities and pursue greater vertical integration, competition across the supply chain will intensify. However, suppliers that can deliver high-voltage solutions and strong system integration capabilities are likely to secure a significant advantage in the next wave of EV electrification.

For more information on reports and market data from TrendForce’s Department of ICT Applications Research, please click here, or email the Sales Department at TRI_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit our blog at https://www.trendforce.com/news/