Global Smartphone Production Reaches 1.25 Billion Units in 2025, with Apple and Samsung Tied for Top Spot, Says TrendForce

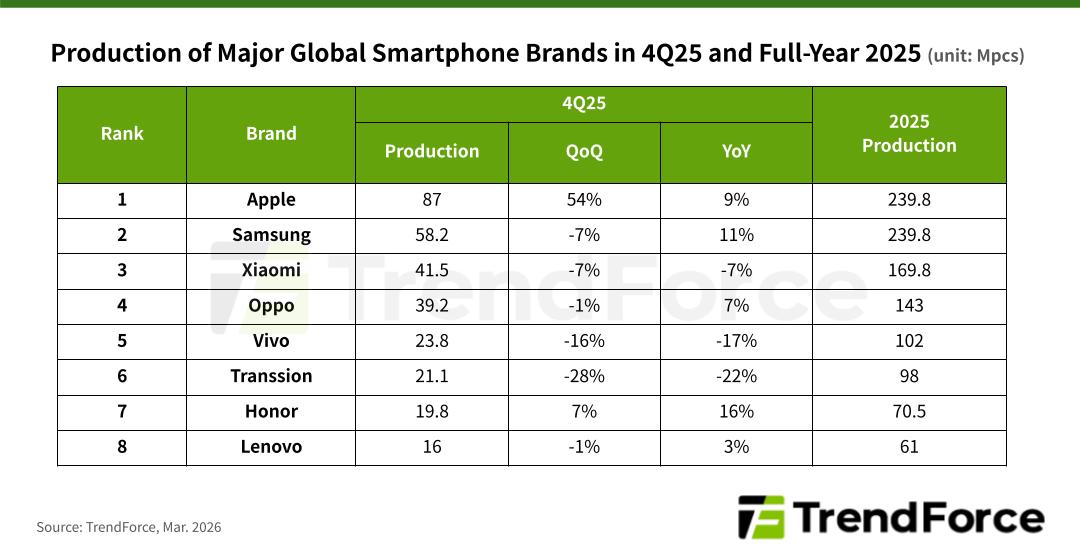

Global smartphone production reached 337 million units in 4Q25, rising 2.7% QoQ, and was supported by strong shipments of Apple’s new iPhone lineup, according to TrendForce’s latest insights into the smartphone industry. For the full year, both Apple and Samsung each produced nearly 240 million units, tying for the top position in global smartphone production.

TrendForce notes that the smartphone market in 1H25 benefited from China’s subsidy programs, while 2H25 was supported by the traditional seasonal peak, bringing total production to approximately 1.254 billion units, up 2.5% YoY.

Looking ahead to 2026, surging memory prices are expected to increase smartphone production costs significantly. As a result, global smartphone output is projected to decline at least 10% YoY to around 1.135 billion units. Smartphone brands will face a difficult choice between raising prices to preserve margins or lowering specifications to sustain shipment volumes, with the entry-level segment expected to bear the brunt of the impact.

In 2025, the iPhone 17 series benefited from well-positioned retail pricing to deliver strong market performance. Apple’s smartphone production in 4Q25 hovered around 8.7 million units, representing more than 50% QoQ growth and marking a new quarterly record. If Apple adopts a more aggressive pricing strategy in 2026, it could help sustain both production and sales momentum.

Samsung produced approximately 58.2 million smartphones in 4Q25, an 11.1% YoY increase. With a higher proportion of premium models and strong vertical integration across the supply chain, Samsung may maintain or potentially expand its market share in 2026 by delaying price hikes and limiting the magnitude of retail price increases.

Xiaomi (including Redmi and POCO) ranked third globally in 2025 with annual production close to 170 million units. In 4Q25, Xiaomi reduced output by around 7% QoQ, partly to adjust inventory from the previous quarter and partly due to its high exposure to entry-level devices. This prompted early production adjustments in response to rising memory prices. In 2026, Xiaomi is expected to increase the proportion of mid- to high-end models to stabilize profitability.

Oppo (including OnePlus and Realme) ranked fourth with 143 million units produced in 2025. Because Realme focuses on low-cost, high-performance devices that are particularly sensitive to component price increases, the group began reducing the share of Realme’s entry-level models toward the end of 2025 to stabilize overall operations.

Vivo (including iQOO) ranked fifth. The company adopted a cautious production strategy in 4Q25, reducing output by roughly 16% QoQ, primarily due to soaring memory prices and intensified competition from Huawei’s Nova series.

Transsion (including TECNO, Infinix, and itel) ranked sixth, sharply cutting smartphone production in 4Q25 to 21.1 million units, a 28% QoQ decline. Given the brand’s strong focus on entry-level models, this reduction in production could help relieve inventory pressure while preparing for a potential demand slowdown in emerging markets.

Honor, which ranked seventh, accelerated production toward the end of 2025, driving 7% QoQ growth in 4Q25. However, the company, along with Xiaomi, Oppo, and Vivo, will face dual pressure in 2026 from intensifying competition with Huawei and rising memory costs.

Lenovo (including Motorola) ranked eighth globally, producing approximately 61 million smartphones in 2025. Production in 4Q25 remained largely flat compared with the previous quarter. In 2026, Lenovo’s production adjustment is expected to be relatively limited, supported by its operator-driven sales channels and the company’s large PC business, which helps secure a more stable memory supply.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email the Sales Department at SR_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit https://www.trendforce.com/news/