Popular Keywords

Western Digital

News

[News] Western Digital Reportedly Bets $1B on Japan R&D to Power Next-Gen HDDs for AI

With AI driving unprecedented demand for data storage, Western Digital, the world’s largest hard-disk drive (HDD) maker, has announced plans to invest $1 billion in Japan over the next five years, according to Nikkei. CEO Irving Tan, as cited by the outlet, said the investment is aimed at “drivi...

News

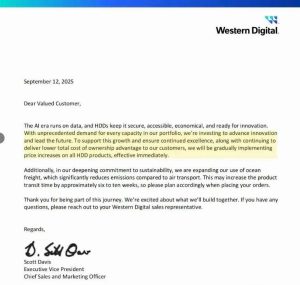

[News] Western Digital Raises HDD Prices Amid Soaring Demand, Shipping Delays of Up to 10 Weeks

Following SanDisk’s 10% NAND price hike and Micron’s week-long pricing freeze, Western Digital has become the third company to act, notifying customers that it will gradually raise prices on all HDD products effective immediately, according to industry sources. According to the notice spotted...

News

[News] WD Sets Flash Business Split Date, Unveils High-Bandwidth Flash as NAND’s Next Leap

Memory giant Western Digital has confirmed the date for the planned separation of its flash business, set to complete on February 21, 2025, according to its press release. Western Digital currently oversees two main divisions, the hard disk drives (HDD) and flash. A previous report from Blocks an...

News

[News] Western Digital’s NAND Flash Division Head to Step Down in Early 2025 ahead of Spin-off

Ahead of Western Digital’s upcoming spin-off, a major personnel shake-up has already taken place, as the memory giant's Executive Vice President and General Manager, Robert Soderbery, who leads the NAND and SSD business unit, will step down on January 2, according to a report from Blocks and Files...

News

[News] WD to Spin Off NAND and SSD Business, with a Valuation Reportedly up to USD 22 Billion

According to the reports from EETimes China and Blocks &Files, Western Digital (WD) is said to be considering spinning off its NAND and SSD business, which could be valued similarly to Solidigm. Reportedly, WD plans to split into two separate business units: one focused on producing hard...

- Page 1

- 5 page(s)

- 25 result(s)