Popular Keywords

PSMC

News

[News] PSMC Joins Intel, SAIMEMORY to Demo 9-Layer Via-in-One Architecture for High Bandwidth 3D Memory

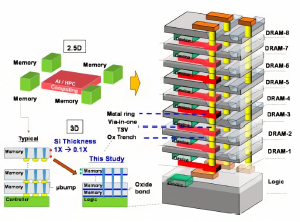

As Intel's collaboration with SoftBank subsidiary SAIMEMORY on Z-Angle Memory (ZAM) continues to draw intense industry attention, new details are emerging ahead of the VLSI Symposium 2026 scheduled for June. According to a pre-release summary leaked from the VLSI official session listing, Taiwan�...

News

[News] PSMC Raises DRAM and NAND Prices in Mar–Apr; Micron and Intel EMIB Programs Reported to Advance

While PSMC swung back to profit in Q1 amid surging memory demand, the Taiwanese chipmaker has also been lifting prices across multiple product lines. Citing company president Martin Chu, Liberty Times reports that PSMC sharply raised DRAM foundry pricing in March, while NAND flash wafer start prices...

News

[News] PSMC Core Business Reportedly Swings to Profit in Q1; Micron Deal Adds Strategic Upside

Following Micron’s completion of its acquisition of Powerchip Semiconductor Manufacturing Corp’s Tongluo P5 fab in March, the Taiwanese chipmaker provided further operational updates. According to Central News Agency, PSMC said at its annual general meeting on April 10 that first-quarter operati...

News

[News] Micron Reportedly Schedules March 26 Tool Move-In at PSMC Tongluo Fab, Signaling Next Deal Phase

After formally signing an exclusive letter of intent to acquire Powerchip Semiconductor Manufacturing Corp. (PSMC)’s P5 fab in Tongluo for US$1.8 billion, Micron has begun moving the deal forward. According to TechNews, the memory giant recently sent out a confidential invitation announcing a tool...

News

[News] Israel Unrest Disrupts Tower; Orders Reportedly Shift to Vanguard, PSMC, Lifting Mature-Node Pricing

As Israel enters a state of emergency, shipments from Israel-based foundries have reportedly been disrupted, prompting global companies to shift orders. According to Economic Daily News, Israel’s largest foundry and a top-ten global player, Tower Semiconductor, has faced shipment constraints, lead...

- Page 1

- 12 page(s)

- 60 result(s)