Popular Keywords

NAND

Insights

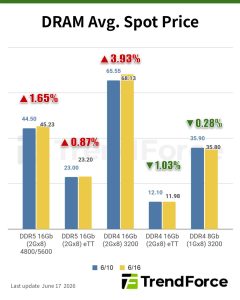

[Insights] Memory Spot Price Update: DRAM Spot Prices See Gains in Low-Density DDR4 and DDR3 Amid Sideways Market

According to TrendForce’s latest memory spot price trend report, DRAM spot prices this week have seen upward momentum in low-density DDR4 and DDR3 segments, while the broader market continues to trend sideways. In NAND Flash, suppliers are adjusting quotations to optimize inventory levels, but buy...

Insights

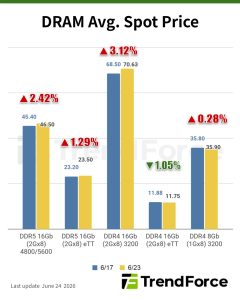

[Insights] Memory Spot Price Update: DRAM Buyers Resist Higher Quotes as Mainstream DDR4 Prices Gain 0.28%

According to TrendForce’s latest memory spot price trend report, DRAM trading remained subdued as buyers showed little willingness to follow higher quotations, with mainstream DDR4 chips (DDR4 1Gx8 3200MT/s) edging up 0.28% this week. In NAND flash, diverging expectations between buyers and seller...

News

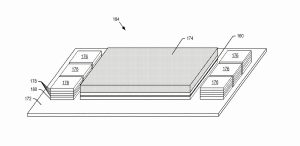

[News] SanDisk Goes Beyond HBF: Patent Bonds Processor onto NAND Tile, with HBM Stacks on Shared Interposer

While SanDisk is speeding up the development of High Bandwidth Flash (HBF), a next-generation architecture that vertically stacks NAND, the company is also advancing additional memory concepts aimed at addressing structural capacity constraints. According to a U.S. patent (US 12,430,274 B2) filed...

Insights

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

News

[News] Key Semiconductor Gas WF₆ Prices Reportedly Surge Over 200% as Supply Tightens Ahead of Japan Output Cuts

While China’s rare earth export controls continue to draw market attention, another key semiconductor material is also seeing sharp price swings. According to chinastarmarket.cn, citing China’s General Administration of Customs, tungsten hexafluoride (WF₆) hit $149.79 per kilogram in April 202...

- Page 1

- 41 page(s)

- 202 result(s)