Popular Keywords

NAND

News

[News] The Race to 400-Layer NAND: Roadmaps and Key Technologies Driving Samsung, SK hynix, and Kioxia

As SK hynix reportedly targets mass production of 375-layer NAND by year-end, according to The Elec, the 400-layer threshold is increasingly seen as a key technical frontier in advanced NAND scaling. Against this backdrop, ET News notes that Samsung began mass producing its 286-layer NAND in Apri...

Insights

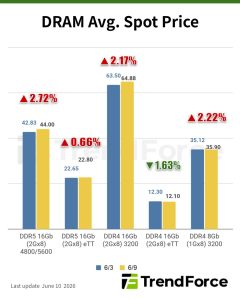

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

News

[News] Laser Annealing Adoption May Broaden with Wolfspeed, Samsung SiC Push and 400-Layer NAND Expansion

Laser annealing adoption appears to be broadening. According to ETNews, the thermal treatment process is expanding beyond its traditional use in silicon (Si) wafers to silicon carbide (SiC), a material widely regarded as a leading candidate for next-generation power semiconductors. The report adds t...

Insights

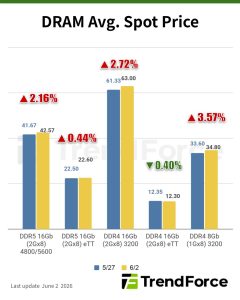

[Insights] Memory Spot Price Update: DDR4 and DDR5 Extend Gains, Though Higher Quotes Temper Procurement Demand

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR4 and DDR5 spot prices continued to rise, with both segments posting notable gains. However, buyers remained cautious amid higher supplier quotes. In the NAND flash segment, spot quotations would continue to slum...

News

[News] Kioxia Targets ¥470B Yearly Capex in FY26–28, Up 66% from FY25, Reportedly Weighing Third Kitakami Fab and M&A

After projecting a 48-fold year-on-year surge in net profit for the April–June quarter, Japan’s NAND heavyweight Kioxia delivered an even more bullish outlook at its Investor Day on June 2. According to EE Times Japan, the company plans to ride the memory upcycle with average annual capital expe...

- Page 2

- 41 page(s)

- 202 result(s)