Popular Keywords

DDR5

Insights

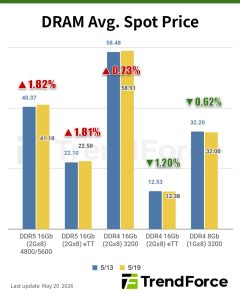

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

Insights

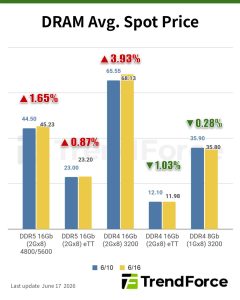

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

Insights

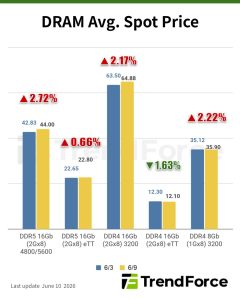

[Insights] Memory Spot Price Update: DDR5 Spot Price Gains Narrow Amid Sluggish Trading; DDR4 Rebounds

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR5 spot price gains narrowed amid sluggish trading, while DDR4 2Gx8-3200 and 1Gx8-3200 prices rebounded after earlier declines. In the NAND flash segment, spot prices are expected to remain under pressure in the n...

Insights

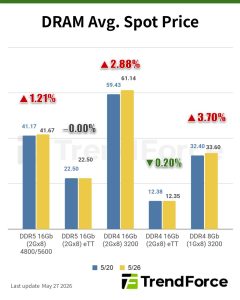

[Insights] Memory Spot Price Update: DDR5 Spots Strengthen on Branded Demand and Higher Bids, DDR4 Weakens

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, DDR5 spot market remained active, with notable inquiries for branded chips, while DDR4 activity stayed subdued. In the NAND flash segment, higher-than-expected 2Q26 contract settlements have provided support to spot...

News

[News] China Memory Module Maker POWEV Advances DDR5 Push as 64GB RDIMM Reportedly Enters Volume Production

As the market focuses on China’s push into HBM and next-gen NAND, another domestic memory player is quietly advancing in DDR5 amid the AI-driven demand surge. According to IT Home and Security Times, module maker POWEV said its 64GB 5600MT/s DDR5 Registered DIMM (RDIMM) server module, launched ear...

- Page 1

- 13 page(s)

- 61 result(s)