Popular Keywords

NAND Flash

News

[News] China’s Memory Sector Booms: 13 A-Share Firms Project Triple-Digit Profit Growth in 2025

As global heavyweights Samsung, SK hynix and Micron cash in on surging prices driven by the AI boom, China’s smaller memory players are also catching the upcycle. According to Sina, as of January 29, 52 A-share memory-related companies had released their 2025 earnings forecasts, with 13 of them pr...

News

[News] SanDisk Beats Forecasts with 600%+ Profit Jump; First LTA Reportedly Sealed as Momentum Builds

While Samsung and SK hynix’s freshly announced record 4Q25 results, NAND giant SanDisk emerges as another major beneficiary amid the AI boom. According to Barron’s, for the December quarter, SanDisk delivered a clear earnings beat, posting adjusted EPS of US$6.20, far above Wall Street’s US$3....

News

[News] Samsung Trails SK hynix for 2025 but Tops Q4 with Record KRW 20T Earnings amid Chip Rebound

Riding the momentum from SK hynix’s impressive results yesterday, Samsung announced on Jan. 29 that fourth-quarter sales jumped 23.8% year on year to KRW 93.84 trillion, while operating profit more than tripled, soaring 209.2% to KRW 20.07 trillion, marking a record-breaking quarter. The strong...

News

[News] Second-Tier No More: Kioxia and SanDisk Balance Alliance and Rivalry in AI NAND Race

Ahead of Samsung and SK hynix’s earnings calls, Micron’s $24 billion Singapore investment is drawing attention, signaling a renewed industry focus on NAND. EE Times reports that as AI workloads shifted from training to inference, SSDs powered by NAND are widely deployed in AI data centers, a tre...

Insights

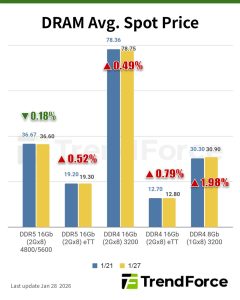

[Insights] Memory Spot Price Update: DDR4/DDR5 Hit Highs, Buyers Hesitant; DDR3 Sees Uptick

According to TrendForce's latest memory spot price trend report, regarding DRAM, rising DDR4/DDR5 prices and challenges in passing on costs have stalled factory procurement, leaving spot market transactions stagnant, yet quotations stay elevated amid ongoing supply shortages. Meanwhile, in NAND, spo...

- Page 17

- 81 page(s)

- 402 result(s)