Rising Costs to Drive Further Increases in EV Cell Prices in 2Q26, Says TrendForce

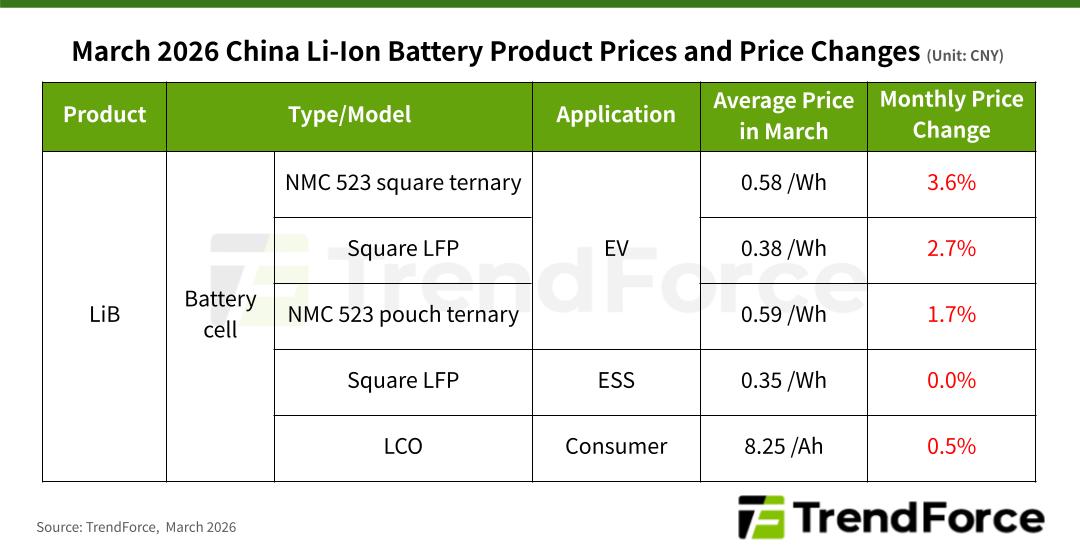

TrendForce’s latest research on the lithium battery industry reveals that surging raw material prices in 1Q26 supported an upward trend in EV battery pricing through March, with average cell prices rising by 1–3% MoM. Among key products, pouch-type ternary cells increased to CNY 0.59/Wh, while square ternary and LFP cells reached CNY 0.58/Wh and CNY 0.38/Wh, respectively.

In March, ESS cell prices remained stable amid strong market demand. Manufacturers reported full order books and high utilization rates. TrendForce expects this demand momentum to extend into the second quarter, supporting stable pricing in the near term, with potential for modest increases moving forward.

At recent energy storage exhibitions in Beijing, newly showcased products were primarily large-capacity cells exceeding 500Ah. A number of leading vendors have already begun volume shipments, while most suppliers remain in the sample delivery stage. Overall production capacity for 500Ah+ ESS cells is expected to gradually ramp up in the third quarter of this year, reaching large-scale mass production around mid-2027.

Geopolitical tensions, including conflicts in the Middle East, intensified energy shortages and price volatility in the first quarter, pushing up battery chemical costs. However, demand trends diverged between the EV and energy storage markets.

EV demand recovery fell short of expectations, with China’s domestic NEV sales declining YoY in the first quarter as well. That being said, rising global oil prices have significantly increased the cost of internal combustion vehicles, improving the cost-performance advantage of EVs and boosting overseas demand. As a result, China’s NEV exports posted strong YoY growth, offsetting weakness in domestic demand.

Meanwhile, the energy storage market remained robust in 1Q26. Ongoing geopolitical risks have heightened the importance of energy security, while supportive subsidy policies across multiple regions, including Europe, the Middle East, and Southeast Asia, have driven strong growth in residential and commercial & industrial (C&I) storage demand. Overall, demand for energy storage cells remains solid.

Looking ahead to 2Q26, rising costs for chemical materials and non-ferrous metals such as copper, aluminum, and lithium are expected to further drive-up overall battery costs. On the demand side, energy storage is likely to remain strong, while the EV battery market continues a gradual recovery. Consequently, cell prices are expected to remain stable with an upward bias, with average prices likely to continue edging higher.

For more on the latest technology industry news and trends, please visit News.