Smartphone Production Registers Largest YoY Drop on Record with 16.7% Decline in 2Q20, Although Rebound in 2H20 Appears Likely, Says TrendForce

The COVID-19 pandemic has compelled governments worldwide to impose border closures and regional lockdowns, which led to significant declines in various countries’ GDPs this year. As economic and social activities around the world have stagnated, the performance of the smartphone industry was severely damaged in 2Q20. According to TrendForce’s latest investigations, total smartphone production reached 286 million units in 2Q20, a slight QoQ rebound of 2.2%, but a 16.7% decrease YoY, which is the largest quarterly YoY drop in history.

TrendForce indicates that governments in many countries have started to ease some of the restrictive measures for containing COVID-19 and launched economic stimulus policies to generate consumer demand. These developments will be beneficial for the smartphone market’s potential rebound going into the second half of the year. Total smartphone production for 3Q20 is expected to reach 335 million units, a 10.1% decrease YoY. Although this figure falls short compared with the same period last year, it still represents a 17.2% increase QoQ.

Samsung was the only manufacturer among the top six to see its market share decline in 2Q20, while Huawei’s market share in China may be cannibalized by its competitors

In the course of the COVID-19 pandemic since March, the situation has gotten worse for most countries. Europe, the US, and India are the major markets for Samsung smartphones when looking at sales by region. Their outbreaks were very severe during 2Q20, and this affected Samsung more than the other brands in the top six. Although Samsung led the industry in terms of smartphone production with 55 million units in 2Q20, it is also the only brand among the top six that posted a QoQ decline, which approached 16%. Moving to 3Q20, as China-U.S. tensions intensify due to the latter's sanctions against Huawei, and China-India relations continue to destabilize, Samsung has been building up its inventories as it targets the entry-level and mid-range segments in order to compensate for its poor performances in the previous quarter. Samsung’s production volume is likely to increase in 3Q20.

Placing second in the production ranking, Huawei, which continues to heavily rely on the Chinese market, raised its smartphone production by 13% QoQ to around 52 million units for 2Q20. Competition in this market is expected to intensify in 3Q20 as smartphone brands release their new flagship models in 2H20. Huawei’s smartphone sales in overseas markets have been falling sharply since the end of 2019 as the effect of the trade actions by the US government began to take their toll. These measures will make the R&D of in-house mobile processors and sourcing of components much more difficult for this Chinese smartphone brand. Given that Huawei depends on China for smartphone sales, other Chinese brands, including Xiaomi, OPPO, and Vivo, are expected to cut into Huawei’s market share.

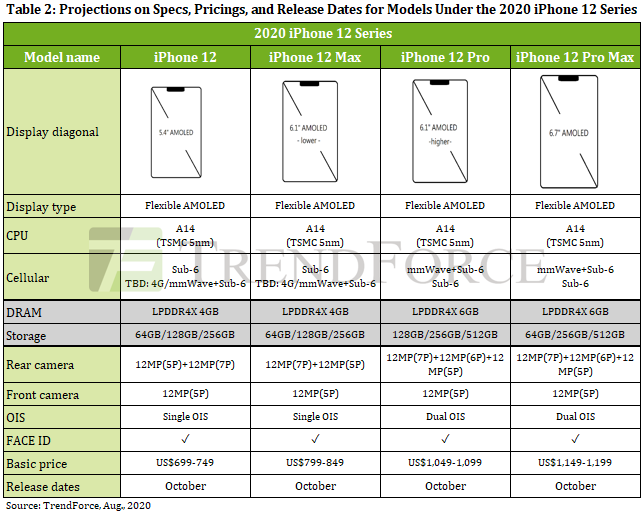

Apple’s iPhone production in 2Q20 rose by 8% QoQ to 41 million units thanks to above-expected sales of the iPhone SE and the iPhone 11. This performance also gives the brand third place in the ranking. Moving to 3Q20, the demand for the iPhone SE and iPhone 11 is expected to remain strong. At the same time, Apple will begin mass producing the four new models in the (tentatively named) iPhone 12 series, which are equipped with 5G capabilities, thereby raising its quarterly smartphone production. The BOM costs of the iPhone 12 models are significantly higher compared with the models in the previous series because of the 5G support. To cut costs and stabilize retail pricing, Apple has decided to sell the upcoming iPhones without accessories such as wired earphones, power adapter, etc. This move is expected to help with sales performance. However, recent orders by the Trump administration barring U.S. businesses from carrying out transactions with TikTok, WeChat, and their respective parent companies ByteDance and Tencent may have an impact on Apple’s sales performances in the Chinese market going forward.

Xiaomi is fourth in the production ranking for 2Q20 with 29.5 million units, OPPO (including OPPO, OnePlus, and realme) is fifth with 27.5 million, and Vivo is sixth with 26.5 million. The three Chinese brands benefitted from the recent recovery of their home market. Furthermore, they also took advantage of the precautionary inventory building in the overseas retail channels during the first half of the year. Retailers stocked up aggressively during that time in fear of pandemic-related disruptions. As a result, they all posted an increase of more than 10% QoQ for 2Q20. Recent border tensions between India and China have placed considerable pressure on the three brands’ sales efforts since they all count on India as one of their major foreign markets. On the other hand, they have been cultivating their presence in the country for a long time. This, combined with their products’ price competitiveness, may be enough to get them through this difficult period with their market shares relatively intact. Nevertheless, Chinese smartphone brands will be very constrained in terms of growth if the relationship between their home country and India remains tense. Xiaomi, OPPO, and Vivo will continue to prioritize the entry-level and mid-range segments in their overseas expansion strategies, which include regions such as Europe, India, Southeast Asia, and Russia, over the long term. In China, the three brands will capitalize on the Chinese government’s push to commercialize 5G services by being more proactive in the development and pricing of 5G smartphones.

Smartphone market will likely see a rebound in production and a sharp rise in 5G penetration in 2021

TrendForce forecasts a yearly smartphone production volume of 1.24 billion units for 2020, an 11.3% decrease YoY. Assuming the pandemic can be brought under control in 2021, total smartphone production is likely to make a rebound next year. As well, smartphone brands are pushing out 5G models this year to maintain their market shares in the face of the recent demand slump. Since mobile SoC suppliers such as Qualcomm and MediaTek are also starting to provide 5G solutions for mid-range and high-end smartphones, the share of 5G models in the annual total smartphone production is projected to grow rapidly to 19.2% for 2020. This penetration rate is equivalent to around 238 million units.