[News] Micron Earnings Preview: Four Key Areas in Focus — HBM Progress, Capex and More

As Micron prepares to report its fiscal third-quarter results on June 24, investor attention is turning to whether its strong earnings and elevated margins can be sustained, and how long the ongoing memory rally can support its growth story in DRAM and HBM. Here are four key areas to watch in the upcoming earnings of the U.S. memory giant.

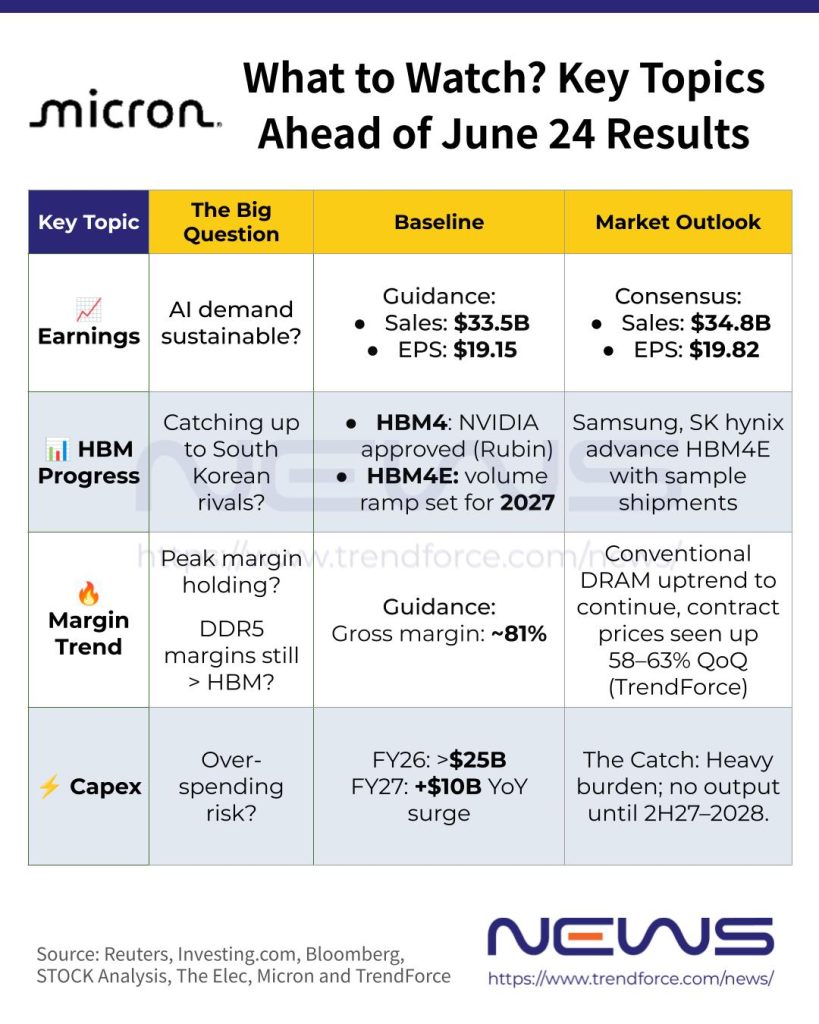

Earnings Preview: EPS Poised for Over 60% Jump

In March, Micron guided fiscal third-quarter revenue of $33.5 billion, plus or minus $750 million, well above the $24.29 billion consensus, according to LSEG data cited by Reuters. Based on second-quarter revenue of $23.86 billion, this implies roughly 40% quarter-on-quarter growth.

According to Investing.com, Micron’s fiscal third-quarter earnings are expected to show a strong step-up, with consensus estimates at about $19.82 per share on roughly $34.8 billion in revenue — a marked increase from $12.20 per share in the prior quarter. The report also links the projected growth to rising HBM demand and gross-margin guidance near 81%.

Tangible Progress in HBM4 and HBM4E in Focus

Meanwhile, attention is turning to whether Micron will provide more concrete updates on HBM4 and next-generation HBM4E developments. As reported by Bloomberg, NVIDIA CEO Jensen Huang said in early June that all three major memory suppliers have secured approval for HBM4 supply for Vera Rubin.

Beyond HBM4, the industry is also advancing toward HBM4E, which is expected to power NVIDIA’s Rubin Ultra. Samsung led the race by shipping HBM4E samples in late May, followed shortly by SK hynix in mid-June. As both giants push forward their advanced roadmaps, they are targeting a pin speed of up to 16Gbps (with Samsung delivering a stable 14Gbps scalable to 16Gbps) for HBM4E.

Micron has also offered early clues about its own roadmap. Speaking at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference in May, Global Operations EVP Manish Bhatia said the company’s first HBM4E product will be based on the JEDEC standard, with volume ramp expected in 2027, according to a STOCK Analysis transcript.

While Micron currently uses 1-beta DRAM for HBM4, Bhatia said the company plans to transition to 1-gamma DRAM in the HBM4E generation. He also confirmed that logic dies for both standard and custom HBM4Es are expected to be manufactured by TSMC.

The shift would place Micron alongside Samsung and SK hynix in advancing to more sophisticated DRAM nodes for next-generation HBM, with both rivals already adopting 1c DRAM as the core die for HBM4E.

Can Micron Sustain Its Peak Margins?

Micron’s guided 81% gross margin for the fiscal third quarter, if realized, will serve as a bellwether for the sustainability of the memory price rally. During the previous earnings call, Micron CEO Sanjay Mehrotra, according to The Elec and Investing.com, noted that “non-HBM margins are currently higher than HBM.”

As noted by The Elec, this implies that DDR5 profitability has now overtaken HBM, underscoring how much Micron’s margins are benefiting from the broader DRAM upcycle.

That tailwind is unlikely to fade in the near term, potentially continuing to support Micron’s profitability. TrendForce expects DRAM pricing momentum to remain intact, following a surge in conventional DRAM contract prices of roughly 93%–98% QoQ in 1Q26. Another 58%–63% QoQ increase is projected for 2Q26, driven by stronger customer willingness to accept price hikes and secure supply allocations, according to TrendForce.

Heavy Capex Raises Margin Concerns

Micron’s aggressive capacity expansion is not expected to translate into meaningful output until the second half of 2027 into 2028, raising questions over the near-term burden of its rising capital spending.

According to an earlier Bloomberg report, Micron has already signaled a sharp increase in capital spending as it ramps up to capture surging demand. The company expects capex to exceed US$25 billion in the fiscal year ending in August, above analysts’ estimate of US$22.4 billion, as per Bloomberg. It also projected fiscal 2027 spending to rise by more than US$10 billion from the prior year, pointing to a multi-year investment cycle, Bloomberg added.

CEO Sanjay Mehrotra previously said the company expects fiscal 2027 capex to “step up meaningfully.” With further guidance due on June 24, investors will be watching closely for any updates on the scale and pace of spending, as well as potential implications for margins and profitability.

Read more

- [News] Micron More Upbeat on Outlook, Reportedly Sets 2027 HBM4E Ramp with TSMC for Standard, Custom Logic Dies

- [News] Micron Says AI Still in Early Stage as Memory Demand Reportedly Seen Exceeding 50% of Total Market This Year

(Photo credit: Micron)