Smartphone Market Bulletin - Dec. 11, 2025

Last Modified

2025-12-11

Update Frequency

Biweekly

Format

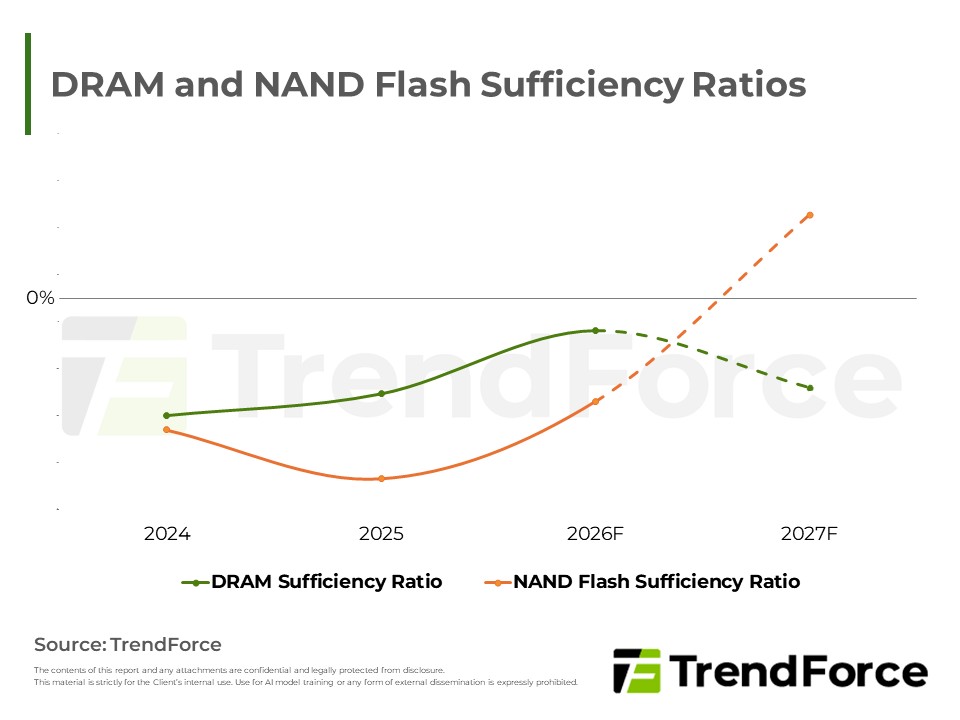

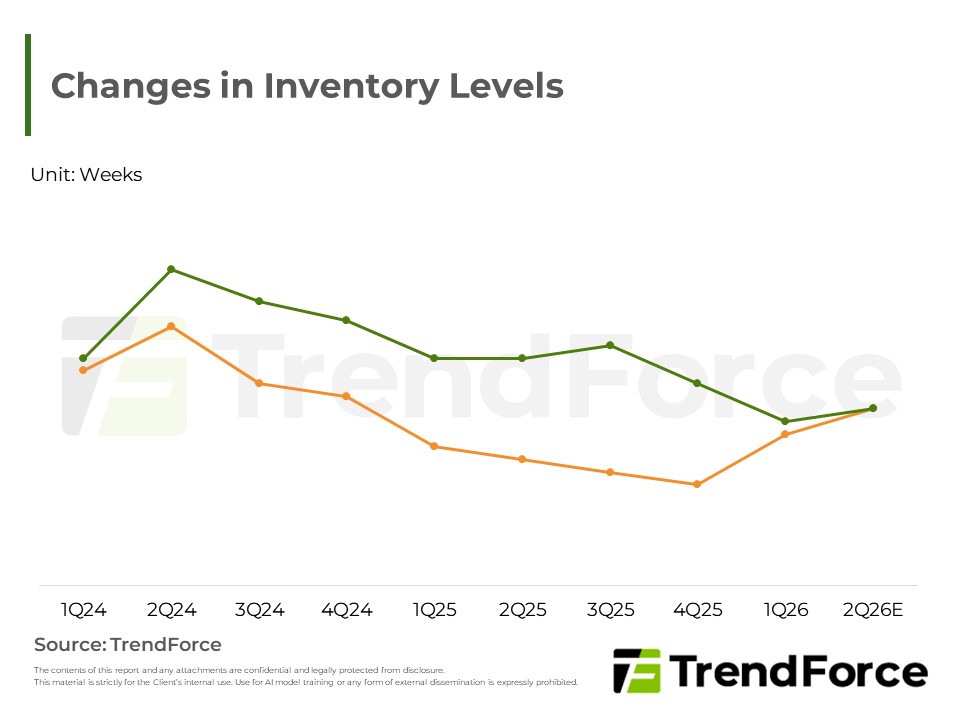

In 4Q25, memory price increases for Chinese smartphone OEMs surpassed those for US OEMs, prompting suppliers to implement "catch-up" price hikes for US clients in 1Q26 to balance regional price disparities. While initial estimates suggest absolute pricing for Chinese clients may remain slightly lower than for US clients, the possibility of expanded hikes due to delayed or combined negotiations with 2Q26 remains. This wave of memory price increases has far exceeded expectations, significantly driving up smartphone BOM costs. Under this immense pressure, brands are compelled to raise prices on new devices, scale back promotions, or accelerate the EOL of older models to maintain operational quality and cash flow.

Key Highlights

- Market Trend: In 4Q25, mobile DRAM/NAND Flash contract prices exhibited a trend of being "higher in China and lower in the US." Starting in 1Q26, suppliers are implementing "catch-up" price increases for US clients to narrow the price gap with Chinese clients and maintain the overall upward pricing trend.

- Mobile DRAM Pricing: Initial estimates suggest that absolute pricing for Chinese clients may remain slightly lower than for US clients. However, further price hikes cannot be ruled out if negotiations are delayed or combined with 2Q26 contract discussions.

- Cost Impact: The rise in memory prices in 1Q26 has exceeded expectations, rapidly amplifying the impact on Bill of Materials (BOM) costs. This signifies that brands must accelerate adjustments to both pricing and product structures to mitigate the impact on profitability.

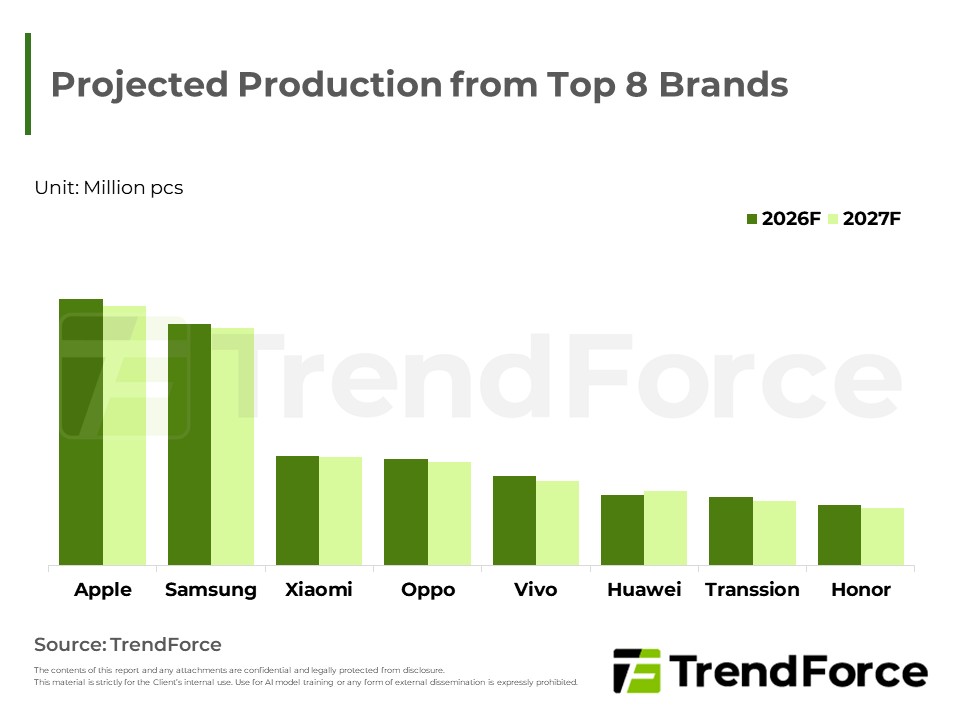

- Apple's Strategy: Despite its strong brand equity and pricing premiums, Apple will need to adjust its pricing strategy. Projections indicate Apple may reduce or cancel price cuts on older models and re-evaluate pricing for new products, potentially raising starting prices to offset cost pressures.

- Android Market Pressure: For mid-to-low-end Android models, memory costs are projected to exceed 40% of the total cost in 1Q26. This forces brands to raise prices on new models, increase prices or reduce promotions on older models, and accelerate the End-of-Life (EOL) process for older devices. Consequently, resources will be concentrated on mid-to-high-end products with higher Average Selling Prices (ASP) to maintain profitability and cash flow.

Table of Contents

- Key Points

- Updates on Smartphone Market

- 1Q26 DRAM and NAND Flash Contract Prices for Android Smartphone Brands

- Price Trends of Smartphones from US Brands

<Total Pages: 4>

Category: Smartphones

Spotlight Report

-

DRAM Monthly Datasheet Jul. 2026

2026/07/22

Consumer Electronics

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Consumer Electronics

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Consumer Electronics

PDF

-

2Q26 Mobile Datasheet

2026/05/29

Consumer Electronics

EXCEL

-

Mobile DRAM Industry Analysis-2Q26

2026/06/05

Consumer Electronics

PDF

-

High-Cost Memory Shuffles Smartphone Market; Global Output Set to Plung

2026/05/29

Consumer Electronics

PDF

Smartphone Market BulletinRelated Reports

Download Report

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jul. 2026

2026/07/22

Consumer Electronics

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Consumer Electronics

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Consumer Electronics

PDF

-

2Q26 Mobile Datasheet

2026/05/29

Consumer Electronics

EXCEL

-

Mobile DRAM Industry Analysis-2Q26

2026/06/05

Consumer Electronics

PDF

-

High-Cost Memory Shuffles Smartphone Market; Global Output Set to Plung

2026/05/29

Consumer Electronics

PDF