Smartphone Production May Drop Over 15%: 2026 Memory Surge Ignites Cost Storm

Last Modified

2026-01-23

Update Frequency

Aperiodically

Format

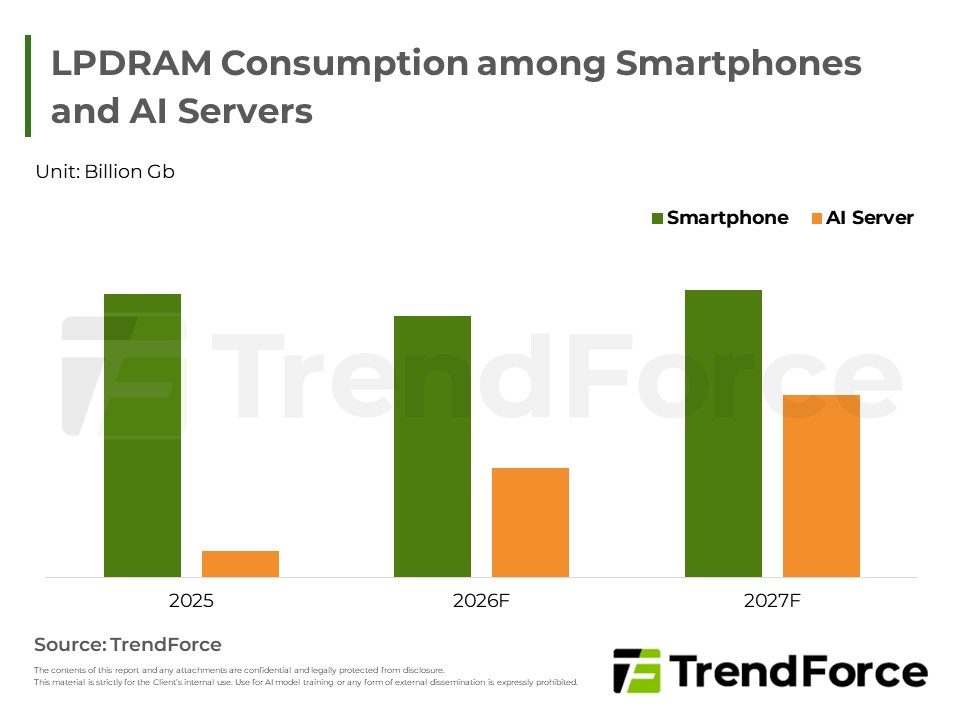

Driven by robust demand for AI servers and high-performance computing, the memory market has entered a super-cycle of price hikes starting from 2H25. Escalating memory costs are forcing brands to raise end-device prices and scale back low-end models to cope with cost pressures. Against this backdrop, the year-on-year decline in global smartphone production for 2026 could widen to approximately 15%, or potentially even higher, under a pessimistic scenario. However, given the absence of signals indicating a halt in price increases and persistent supply tightness, most brands are choosing to maintain their established procurement volumes with suppliers to secure resource allocations. It is noteworthy that this wave of memory price increases is driving up the retail prices of various electronic devices, further evolving into a broader risk of consumer electronics inflation.

Key Highlights

- Memory price hikes in 1Q26 are expected to surpass those of 4Q25, with no signs of the rally stalling for the remainder of the year. The cumulative price increase since 3Q25 has far exceeded expectations, leading to surging costs that threaten to further exacerbate the deterioration of smartphone production performance.

- Given that smartphone gross margins are already thin, brands can no longer absorb these costs or compress marketing budgets to cope. Consequently, they are forced to maintain operations by raising retail prices, reducing the proportion of low-end models, and restructuring their high, mid, and low-end product mixes.

- Despite the downward pressure facing the overall smartphone industry, most brands are opting to uphold their existing Long-Term Agreements (LTAs). Amidst unceasing price hikes and continued supply tightness, this strategy aims to secure future quotas and available resources.

- This memory super-cycle is primarily impacting mid-to-low-end products and brands highly dependent on single markets. Under a pessimistic scenario, total global smartphone production volume in 2026 faces a potential downward revision of approximately 15%, or even steeper.

- The super-cycle of memory price increases is cascading downstream through price adjustments across various electronic devices, diffusing into more comprehensive inflationary pressure within the consumer electronics sector.

Table of Contents

- Smartphone Production Could Continue to Deteriorate in 2026 amidst Incessant Price Hikes on Memory

- Smartphone Memory Price Forecast

- No Adjustments to LTAs among Smartphone Yet under Unchanged Constraints in Memory Supply and Demand

- Soaring Memory Prices Hit Mid-to-Low-End Models Hardest, Placing Them Under Greatest Cost Pressure

- Smartphone Production Forecast

- Memory Super-Cycle Price Hikes May Trigger Inflation Risks in Consumer Electronics

<Total Pages: 7>

Category: Smartphones , DRAM , Semiconductors

Spotlight Report

-

DRAM Monthly Datasheet Jul. 2026

2026/07/22

Consumer Electronics

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Consumer Electronics

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Consumer Electronics

PDF

-

2Q26 Mobile Datasheet

2026/05/29

Consumer Electronics

EXCEL

-

Mobile DRAM Industry Analysis-2Q26

2026/06/05

Consumer Electronics

PDF

-

High-Cost Memory Shuffles Smartphone Market; Global Output Set to Plung

2026/05/29

Consumer Electronics

PDF

Mobile PackageRelated Reports

Download Report

2,000

Membership

- Mobile Package

- Selected Topics New

- Selected Topics-TF-0111_Smartphone Production May Drop Over 15%: 2026 Memory Surge Ignites Cost Storm

Spotlight Report

-

DRAM Monthly Datasheet Jul. 2026

2026/07/22

Consumer Electronics

EXCEL

-

NAND Flash Monthly Datasheet Jul. 2026

2026/07/15

Consumer Electronics

PDF

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Consumer Electronics

PDF

-

2Q26 Mobile Datasheet

2026/05/29

Consumer Electronics

EXCEL

-

Mobile DRAM Industry Analysis-2Q26

2026/06/05

Consumer Electronics

PDF

-

High-Cost Memory Shuffles Smartphone Market; Global Output Set to Plung

2026/05/29

Consumer Electronics

PDF