Global EV Traction Inverter Installations Remain Resilient in 1Q26 Despite Seasonal Slowdown; High-Voltage Architectures Emerge as Key Growth Driver, Says TrendForce

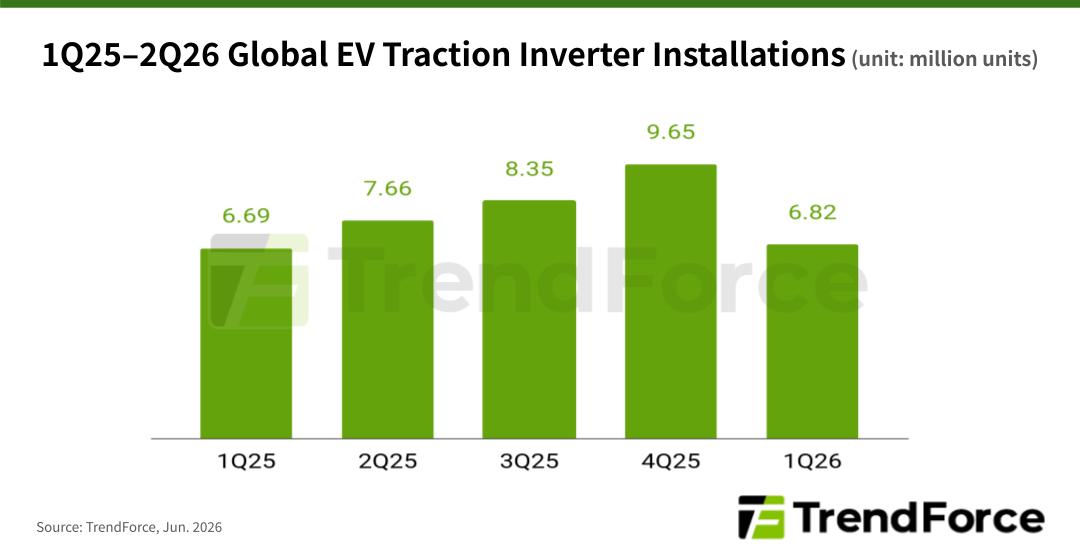

TrendForce's recent report on EV traction inverters shows that in the first quarter of 2026—usually the industry's slowest season—global installations hit around 6.82 million units, a 1.9% increase from 6.69 million units in the same period of 2025. These figures suggest that the electrification push continues strongly despite lower seasonal demand, highlighting the EV market's resilience.

Global traction inverter installations reached approximately 32.35 million units in 2025, representing 18.9% growth from 27.21 million units in 2024. TrendForce forecasts installations to rise further to 36.4 million units in 2026, reflecting annual growth of 12.5%.

Regionally, China's EV sales declined 19% YoY during the quarter, while Western Europe recorded 28% growth, making it the primary contributor to the global market expansion.

BEVs remained the dominant platform for traction inverter deployment, with installations reaching approximately 3.49 million units in 1Q26. This accounted for about 51% of total installations. PHEVs and REEVs contributed approximately 1.65 million units, while HEVs accounted for roughly 1.68 million units. These figures underscore the continued coexistence of multiple electrification technologies across the automotive market.

The industry's migration toward higher-voltage architectures remains evident. Installations of systems operating above 550V, which are typically associated with 800V vehicle platforms, reached approximately 920,000 units in 1Q26. This represents a 21% growth from 760,000 units a year earlier.

Meanwhile, silicon carbide (SiC) MOSFET-based traction inverter installations increased 7.4% YoY to approximately 1.17 million units. The growing adoption of both high-voltage platforms and SiC-based inverters is helping improve vehicle power efficiency, charging performance, and overall system effectiveness.

TrendForce estimates that the ASP of traction inverters in 1Q26 was approximately US$531 per unit—slightly below $546 in the previous quarter. Notably, pricing remained largely unaffected by recent increases in power semiconductor costs.

Several factors contributed to this stability. Market competition remained intense during the seasonal slowdown, while suppliers continued to benefit from inventories acquired at lower historical costs. Additionally, some vendors appear willing to absorb higher component costs in the short term to preserve market share.

TrendForce cautions that sustained cost pressures could test the profitability of both automakers and suppliers over the longer term. Several automakers have already announced vehicle price increases during 2Q26. Whether these cost increases ultimately translate into higher pricing for traction inverters will become clearer in the next quarterly report.

For more on the latest technology industry news and trends, please visit News.