TCL CSOT’s IJP OLED to Enter Branded Monitor and Notebook Products in 2H26, Challenging Korean Dominance, Says TrendForce

TCL CSOT is aggressively promoting inkjet-printed OLED (IJP OLED) technology as a means of entering the OLED monitor and notebook panel supply chain, according to TrendForce’s findings. Its Gen 5.5 IJP OLED production line has already reached volume production and successfully commercialized medical display panels, while validation programs for branded monitor and notebook products are currently underway. The company’s progress could potentially challenge the long-standing dominance of Korean panel makers in the OLED industry.

TrendForce reports that TCL CSOT is initially testing market demand with a 27-inch UHD IJP OLED monitor produced on its Gen 5.5 line, targeting the professional monitor segment. IJP OLED offers superior power efficiency in high-end business and creator-focused displays when compared with existing QD-OLED and WOLED technologies, making it increasingly attractive to brand vendors. Monitor brands from China, Taiwan, and South Korea are currently evaluating IJP OLED panels, and TCL CSOT is expected to begin mass production of IJP OLED monitor panels in the third quarter of 2026.

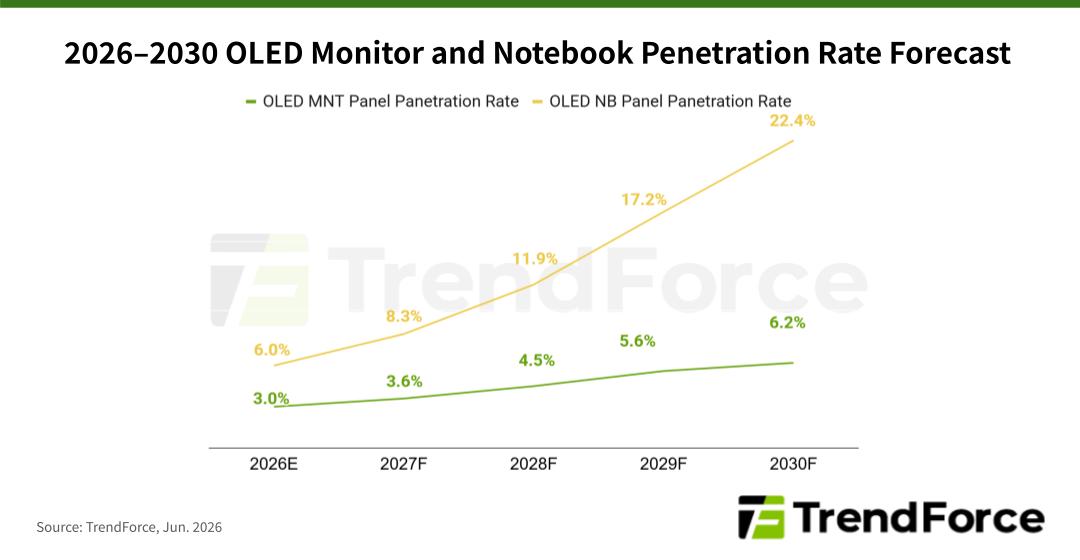

At present, the OLED monitor panel market is effectively dominated by Samsung Display and LG Display. Large-generation OLED capacity remains heavily concentrated among Korean panel makers, limiting OLED monitor penetration to approximately 3% in 2026. However, with TCL CSOT investing in Gen 8.6 OLED production capacity for monitor applications, TrendForce expects OLED monitor penetration to rise to 6.2% by 2030 and continue expanding thereafter.

In the OLED notebook panel market, Samsung Display remains the clear market leader, while China's Everdisplay Optronics has begun to establish a meaningful presence. OLED notebook panel penetration is expected to reach approximately 6% this year.

Unlike the monitor segment, investment in large-generation OLED notebook capacity is becoming increasingly diversified. In addition to Samsung Display, TCL CSOT, BOE, and Visionox have all committed resources to Gen 8.6 OLED notebook panel production. As a result, OLED notebook adoption is expected to accelerate rapidly, with penetration projected to reach 22.4% by 2030.

The commercialization schedule for TCL CSOT's OLED notebook panels may also move ahead of previous expectations. Production, originally targeted for the fourth quarter of 2026, now has the potential to begin as early as the third quarter.

TCL CSOT has chosen a 14-inch WUXGA IJP OLED panel as its entry product for the notebook market, targeting the mid-range and entry-level OLED notebook segments. To appeal to this highly price-sensitive market, the company has adopted an aggressive pricing strategy. Against a backdrop of rising notebook component costs, this approach has already attracted interest from several notebook brands.

Chinese and Taiwanese notebook vendors are expected to be among the first to adopt IJP OLED notebook panels beginning in the third quarter of 2026. Additionally, at least one major U.S. notebook brand is currently conducting qualification testing for IJP OLED notebook products.

For more information on TrendForce’s display reports and market data, please visit the Report Page, or Email (DR_MI@trendforce.com) the Sales Department.

For more on the latest technology industry news and trends, please visit News.