Popular Keywords

DDR3

Insights

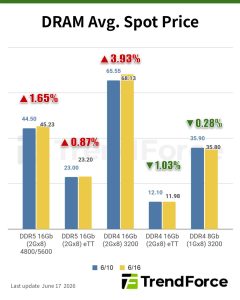

[Insights] Memory Spot Price Update: DRAM Spot Prices See Gains in Low-Density DDR4 and DDR3 Amid Sideways Market

According to TrendForce’s latest memory spot price trend report, DRAM spot prices this week have seen upward momentum in low-density DDR4 and DDR3 segments, while the broader market continues to trend sideways. In NAND Flash, suppliers are adjusting quotations to optimize inventory levels, but buy...

Insights

[Insights] Memory Spot Price Update: DDR3 Strengthens While DDR4 Faces Constraints and Spec Downgrading

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, mainstream DDR4 chips largely traded sideways, while DDR3 spot prices continued to rise, partly supported by tight DDR4 availability and higher costs, which have prompted some consumer DRAM buyers to downgrade speci...

Insights

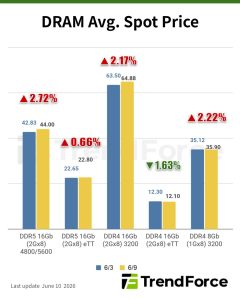

[Insights] Memory Spot Price Update: DDR5 Spot Momentum Continues as DDR4 Tightness Spills Over to DDR3

According to TrendForce’s latest memory spot price trend report, in terms of DRAM, demand for DDR5 is especially strong, while tight supply and persistently high DDR4 prices are pushing some buyers to downgrade to DDR3—lifting DDR3 prices as well. In the NAND flash segment, spot prices have stab...

News

[News] DDR4 Reportedly Leads Legacy Memory Rally with Q1 Prices Up to 50%; DDR3 in Tight Supply

As memory makers increasingly tilt toward server applications, lifting prices for server DRAM and enterprise SSDs, legacy memory is staging a strong comeback of its own. Commercial Times reports that DDR4, DDR3, NOR flash, and SLC/MLC NAND are entering a fresh supply-demand reversal. Among the ma...

News

[News] DDR3 Price Rebound Expected in the Upcoming Quarters, Benefiting Taiwanese Manufacturers

As the standard DRAM market experiences an unprecedented cycle of supply-demand imbalance, the shortage of DDR3 production capacity has become even more severe. According to a report from the Economic Daily News, with leading manufacturers like Samsung exiting DDR3 production, while demand for D...

- Page 1

- 2 page(s)

- 8 result(s)