Popular Keywords

Amazon

News

[News] Amazon Signed Multibillion-Dollar Fiber Optics Supply Agreement With Corning

As investment in AI computing infrastructure continues to accelerate, demand for high-speed optical connectivity in data centers is growing by leaps and bounds. On June 8, Amazon and Corning jointly announced a multiyear, multibillion-dollar agreement under which Corning will supply optical fiber, c...

News

[News] Amazon Weighs In-House Chip Sales as Unit Set to Exceed $20B Annually; Anthropic Explores Custom Silicon

Major tech companies are stepping up efforts to develop in-house chips. Amazon is reportedly exploring the possibility of selling its chips to external customers, while Anthropic is said to be planning its own chip development. According to Bloomberg, Amazon is weighing the option of offering its ch...

News

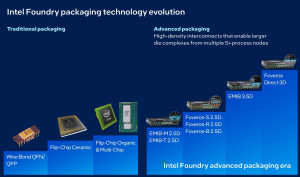

[News] Intel Advanced Packaging Reportedly Gains Traction vs. TSMC as Google, Amazon Weigh EMIB Adoption

Intel’s advanced packaging business is reportedly gaining momentum. According to Wccftech, citing WIRED, sources say the company has been in discussions with at least two major customers—Google and Amazon—on packaging services for ASIC development. This suggests both Google’s TPUs and Amazon...

News

[News] Middle East Escalation Hits Tech: NVIDIA Shuts Dubai Office, AWS Data Center Strike Raises Concerns

In the wake of the U.S.–Israeli military campaign against Iran, technology companies operating in the Middle East are tightening security protocols, with some temporarily shutting offices and modifying regional operations. According to CNBC, NVIDIA temporarily closed its Dubai office, with employe...

News

[News] US Reportedly Mulls Tariff Exemptions for Amazon, Google, Microsoft on TSMC-Made Chips

While many details of the semiconductor duties remain unclear, one certainty is that in January the Trump administration slapped a 25 percent levy on certain AI chips from AMD and NVIDIA. Now, the Financial Times reports that Washington plans to exempt major tech players like Amazon, Google, and Mic...

- Page 1

- 8 page(s)

- 36 result(s)