Popular Keywords

About TrendForce News

TrendForce News operates independently from our research team, curating key semiconductor and tech updates to support timely, informed decisions.

[News] Samsung, SK hynix Reportedly Tapped as NVIDIA Rubin HBM4 Suppliers; Shipments Could Start in March

Ahead of NVIDIA’s GTC next week, all eyes are on the HBM4 supply for its next-gen AI accelerator, Vera Rubin, set for release in the second half of the year. Hankyung, citing industry sources, reports that Samsung Electronics and SK hynix are on the component supplier list. With HBM4 production taking over six months from DRAM wafer to final packaging, the two companies are expected to start production as soon as this month, the report adds.

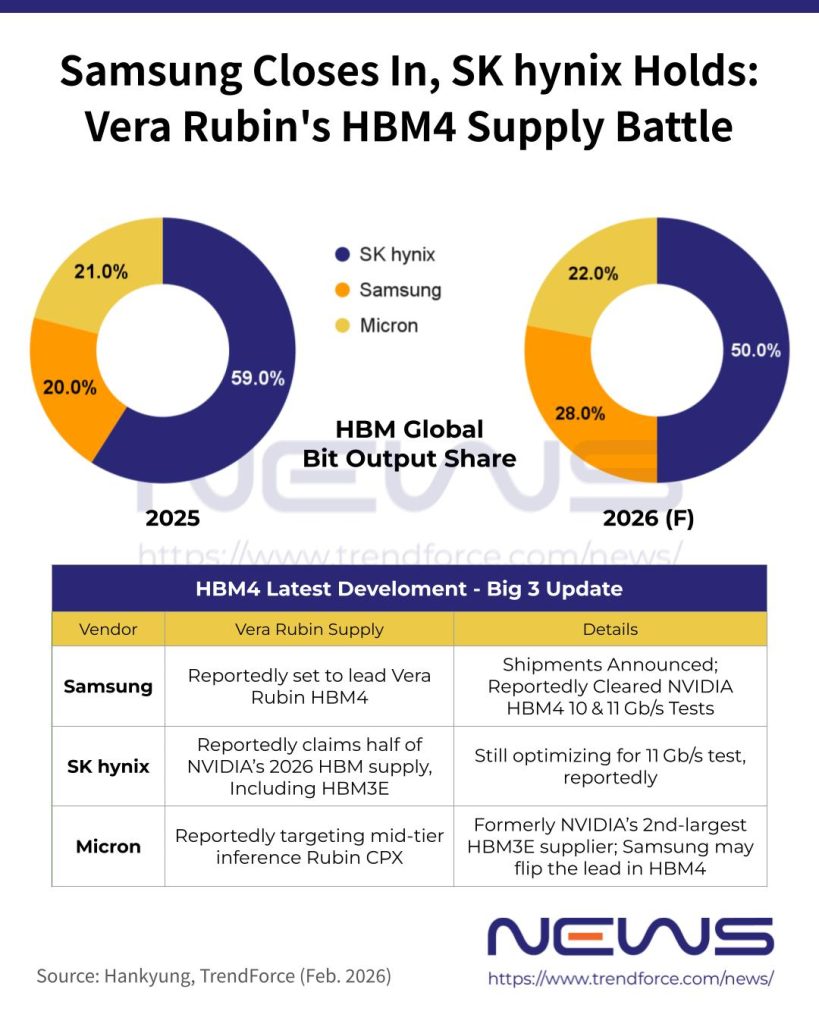

Though allocation and pricing for Vera Rubin’s HBM4 remain unsettled, Hankyung sources expect SK hynix to take over half of NVIDIA’s total HBM supply in 2026, including HBM3E, while Samsung is set to lead Vera Rubin-specific HBM4. According to TrendForce’s projection, SK hynix will still lead global HBM bit output with a 50% share—down from 59% in 2025—while Samsung’s portion climbs from 20% to 28%.

Notably, Hankyung reports that for Vera Rubin, NVIDIA is demanding HBM4 data rates exceeding 10Gb/s, well above the 8Gb/s standard set by JEDEC. According to Hankyung, Samsung has effectively passed NVIDIA’s HBM4 qualification tests, which are being conducted in two tiers at 10Gb/s and 11Gb/s data rates. SK hynix, meanwhile, is still optimizing its product to pass the 11Gb/s test, the report adds.

Hankyung reports HBM4, the AI server memory, stacks 8–16 DRAM dies on a control base. NVIDIA’s Vera Rubin is expected to pack 16 stacks for 576 GB—outpacing AMD’s upcoming MI450, which tops at 432 GB.

SK hynix and Micron Face HBM4 Pressure

Notably, Global Economic suggests that SK Group Chairman Chey Tae-won will personally attend NVIDIA’s GTC for the first time. Industry sources reportedly say his visit underscores SK’s direct involvement, with Chey taking a hands-on role in overseeing SK hynix’s supply schedules and negotiation talks.

The report notes Samsung Electronics kicked off HBM4 shipments in February, while SK hynix has yet to announce deliveries. Analysts suggest the key differentiator between the two could be HBM4’s data-processing speed.

On the other hand, Hankyung notes that Micron is not entirely out of the HBM4 market, as the company is expected to provide HBM4 for mid-tier AI accelerators geared toward inference, such as Rubin CPX, rather than the flagship Vera Rubin.

Samsung’s Leverage

Notably, as highlighted by TrendForce, prices for conventional DRAM have surged sharply since 4Q25, narrowing HBM’s historical advantage in profitability. Memory vendors are therefore recalibrating capacity allocation between HBM and conventional DRAM to balance overall revenue growth and customer commitments. Under such conditions, NVIDIA’s reliance on a single supplier could hinder the ramp-up of the Rubin platform.

Hankyung also notes that server-grade commodity DRAM modules, such as SOCAMM2, now cost around $1.3 per Gb, reaching levels close to NVIDIA’s flagship HBM3E. From Samsung’s perspective, therefore, producing more commodity DRAM—rather than HBM4, which requires expensive stacked DRAM processes—may be more profitable, the report adds.

As Hankyung notes, Samsung, holding both HBM4 and commodity DRAM, can present NVIDIA with multiple bargaining options.

Read more

- [News] NVIDIA GTC 2026 in Focus: Feynman Reportedly on TSMC A16, Samsung & SK hynix to Showcase HBM4

- [News] NVIDIA May Relax HBM4 Specs as Samsung and SK hynix Reportedly Face Capacity, Yield Limits

(Photo credit: Samsung)

Please note that this article cites information from Hankyung and Global Economic.