[Insights] Late January TV Panel: 32-Inch Leads USD 1 Increase, Signaling Stabilization

According to the latest panel prices released by TrendForce in late January, panel manufacturers continue to implement large-scale production cuts and maintenance plans. Additionally, the shortage of upstream materials for polarizers is affecting the panel prices. 32-inch TV panel prices have seen an increase. Meanwhile, the prices of mainstream sizes for monitor panels are expected to stabilize. Here are the details:

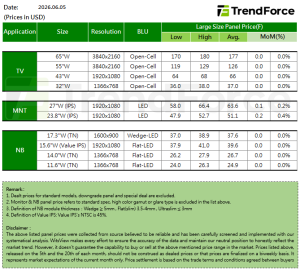

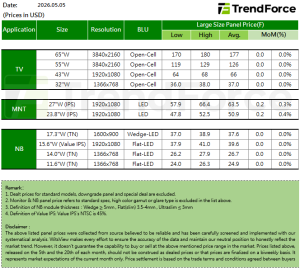

TV

Despite being a slow season for demand in January, panel manufacturers are actively trying to reverse the trend of TV panel price declines through extensive production cuts and maintenance plans.

Recent observations indicate that some Chinese brand customers are increasing their stockpile demand for the North American tax refund season in March-April.

On the other hand, the disruption in the supply of upstream polarizer materials due to the earthquake in Japan at the beginning of the month is also contributing to a stabilization in panel prices. Therefore, the price trend for TV panels in January is expected to see a rise in 32-inch panels, while 43-inch to 75-inch panels are expected to stabilize.

Monitor

Entering January, despite the onset of a slow season for demand, panel manufacturers are encouraging customers to stock up early due to the upcoming Chinese Lunar New Year in February.

Observations indicate that there is limited room for additional orders in the latter part of January. The shortage of upstream polarizer materials is also expected to impact some VA panels. Therefore, in terms of monitor panel prices for January, mainstream sizes such as 21.5 inches, 23.8 inches, and 27 inches are expected to stabilize, while Open Cell panels are expected to have a downward space of USD 0.1 to 0.2.

NB

After entering the first quarter of 2024, laptop panel demand has significantly weakened, as some customers increased their stockpiles at the end of the previous year. Brand customers are requesting panel manufacturers to lower prices, and panel manufacturers are adopting a relatively soft stance, resulting in downward pressure on panel prices.

Observations of laptop panel price trends in January show that 16:10 models, due to their higher unit prices, still have room for continued convergence with 16:9 models. Therefore, it is expected that the prices of 14-inch 16:10 models will decrease by USD 0.2, and 16-inch 16:10 models will decrease by USD 0.3, with a larger decline. Mainstream 16:9 IPS models are expected to decrease by USD 0.1, while 16:9 TN models are expected to remain stable.