Global OLED Monitor Shipments Rose by 78% YoY for 1Q26, Bolstered by the Release of QD-OLED Panel Supply, Says TrendForce

According to the latest research by global market intelligence firm TrendForce, the OLED monitor market entered a seasonal downturn in 1Q26. Moreover, strong promotional campaigns in 4Q25 had already pulled forward demand. Consequently, global OLED monitor shipments dropped by 11% QoQ in 1Q26. However, from a YoY perspective, 1Q26 shipments actually soared by 78%. The key growth driver was the increasingly abundant supply of QD-OLED panels, which enabled new market entrants to ramp up volumes and effectively fill gaps in the market.

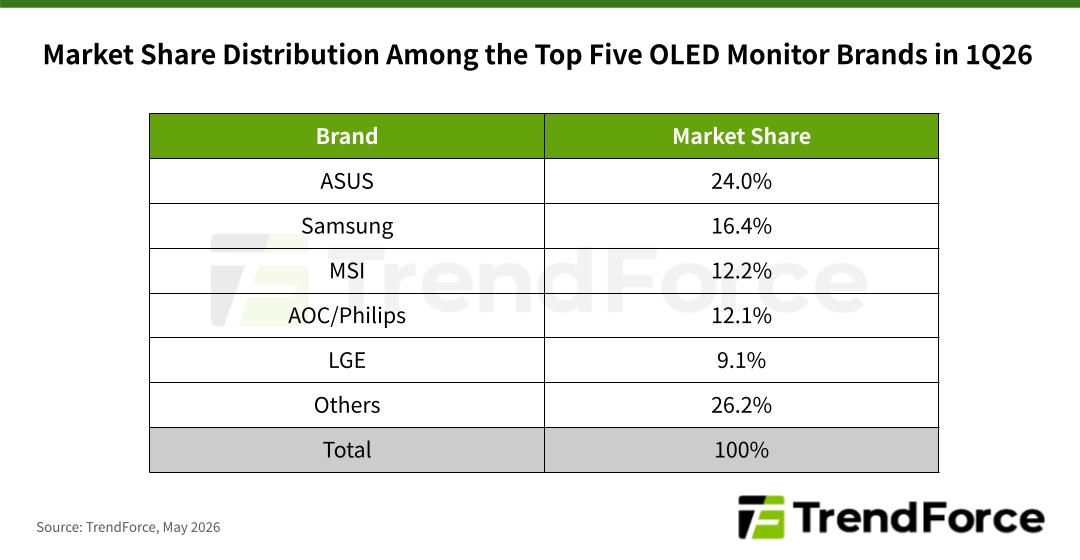

In terms of market share, ASUS remained firmly at the top of the rankings in 1Q26 with a 24% share. Its leadership was underpinned by a comprehensive OLED product lineup. As part of its first-quarter product push, ASUS launched a 34-inch gaming monitor with an ultra-high 360Hz refresh rate and continued to expand into mobile displays with a new 16-inch portable OLED monitor. The brand leverages a highly differentiated product matrix to reinforce its competitive barrier.

Samsung ranked second with a 16.4% share for 1Q26. Backed by ample in-house QD-OLED panel resources and years of experience in the high-end display segment, Samsung maintained strong growth momentum even during the off-season. Its exclusive models—such as the 27-inch QHD 180Hz monitor—continued to perform well, helping to sustain solid shipment levels.

The race for third and fourth place was extremely tight. MSI ultimately edged out AOC/Philips to claim third with a 12.2% share, compared with AOC/Philips’ 12.1%. As competition between the two brands intensifies, their product strategies differ clearly. MSI has benefited from stable shipments of its 31.5-inch models while simultaneously expanding into both commercial and high-end gaming segments. Its 27-inch UHD commercial monitor and 34-inch gaming monitor with a high refresh rate of 360Hz both debuted in the first quarter, and this broader product upgrade helped it secure third place.

In contrast, AOC/Philips has concentrated on the 27-inch QHD segment as its key battleground and used aggressively priced entry-level models to drive volume. Hence, it was able to firmly establish its market position in the first quarter. With its market share now only slightly below MSI’s, the brand held fourth place in 1Q26 while closing in on third. AOC/Philips has emerged as the most formidable challenger in the current rankings.

LGE ranked fifth with a 9.1% share for 1Q26. The company launched an exclusive 39-inch WUHD OLED 165Hz monitor in the first quarter, and the product is expected to contribute significantly to shipments in the second quarter. LGE’s main competitive strength lies in ultra-wide products, which already accounted for 40% of its shipments in 1Q26. As new products gain traction, this share is expected to approach 45% in the second quarter.

For more on the latest technology industry news and trends, please visit News.