Memory Price Surge Disrupts Supply Chain; Global Smartphone Panel Shipments Forecast to Fall 7.3% in 2026, Says TrendForce

TrendForce’s latest research on smartphone panels reveals that shortages and rising memory prices—one of the most costly components in smartphones—are reshaping brand shipment strategies for 2026 and weakening panel demand.

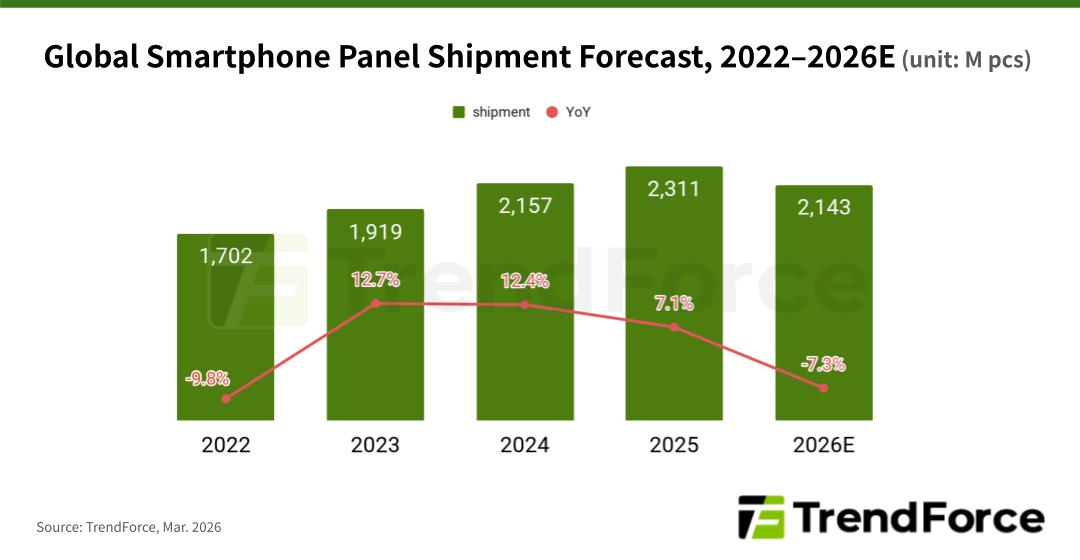

Global smartphone panel shipments are projected to reach 2.14 billion units in 2026, down 7.3% YoY from 2.31 billion units in 2025. This marks the end of the growth cycle that began in 2023 and the market’s first annual decline in several years.

TrendForce notes that procurement of smartphone panels in 2026 will be constrained by softer new handset shipment momentum. The secondary handset market, which previously helped support overall demand, is now facing shipment headwinds as soaring memory costs and supply constraints limit device availability. While demand from the repair market appears relatively stable, cautious consumer spending sentiment is unlikely to offset the slowdown in new handset sales.

The smartphone panel market is showing trends of strong high-end demand, transformation in the mid-range segment, and stability in entry-level models. As low-cost single RAM (RAM-less) AMOLED technology matures, smartphone brands are accelerating the shift from LTPS LCD to AMOLED panels in mid-range devices while focusing resources on premium models, where price sensitivity is lower. TrendForce estimates that AMOLED panels will account for 43.2% of smartphone panel shipments in 2026, up from 41.2% in 2025.

By contrast, LTPS LCD panels are seeing their market share sharply squeezed, with shipments expected to decline from 4.4% in 2025 to 2.5% in 2026. Meanwhile, a-Si LCD panels, which primarily serve entry-level smartphones, are projected to remain relatively stable with approximately 54.4% market share.

As system costs increase due to rising memory prices, smartphone brands might pass some of these costs to consumers. Meanwhile, they are likely to strengthen supply chain cost management to keep retail prices competitive, which could increase pricing pressure on key component suppliers like display panel makers.

LCD panels used in mid- and low-tier smartphones are likely to experience the most significant price declines, as weak demand and ongoing inventory adjustments weigh on the market. Even AMOLED panels, despite their technological advantages, may struggle to maintain pricing stability amid increasingly cautious procurement strategies from smartphone brands and intensified price competition among panel makers seeking to secure orders.

Overall, soaring memory prices have become the largest uncertainty for the smartphone panel market in 2026. How smartphone brands adjust their product mix and inventory levels—and how consumers respond to potential handset price increases versus repair or extended device usage—will be key indicators shaping the industry’s outlook moving forward.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email the Sales Department at DR_MI@trendforce.com

For additional insights from TrendForce analysts on the latest tech industry news, trends, and forecasts, please visit https://www.trendforce.com/news/