Popular Keywords

About TrendForce News

TrendForce News operates independently from our research team, curating key semiconductor and tech updates to support timely, informed decisions.

[News] Applied Materials Teams Up with Micron, SK hynix for Next-Gen DRAM, HBM and NAND Development

As the AI boom drives memory demand, semiconductor equipment makers are reaping the benefits while deepening ties with top memory producers. Applied Materials has teamed up with Micron and SK hynix to develop next-generation chips critical for AI and high-performance computing, according to Reuters.

Applied Materials said in a March 10 press release that it signed a long-term collaboration with SK hynix to accelerate DRAM and HBM development. Reuters also noted that the partnership will focus on advancing memory materials, process integration, and 3D advanced packaging technologies at Applied Materials’ newly established research hub—the Equipment and Process Innovation and Commercialization (EPIC) Center.

Meanwhile, the partnership with Micron targets DRAM, HBM, and NAND, leveraging Applied’s EPIC Center and Micron’s innovation hub in Boise, Idaho, according to the company’s press release.

As highlighted by Reuters, the moves come as Big Tech—including Google, Microsoft, and OpenAI—plans to invest $630 billion in 2026 to expand AI infrastructure, fueling soaring memory demand.

The EPIC Center itself represents a planned $5 billion investment in semiconductor equipment R&D, with spending ramping up alongside customer projects. Notably, in February, Applied Materials also announced that Samsung will join the center, with teams working side by side to fast-track next-generation technologies to market.

Memory: The New Growth Goldmine for Toolmakers

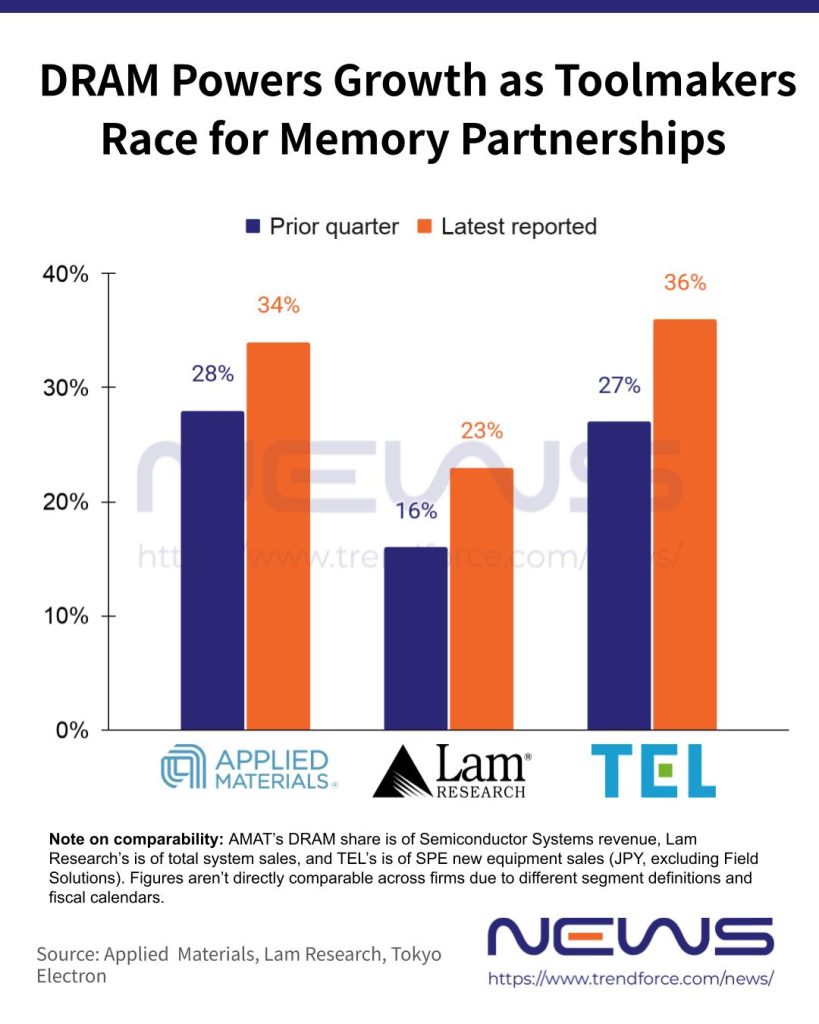

It is worth noting that memory related equipment and materials have emerged as the new growth engine for semiconductor equipment firms. According to Applied Materials’ earnings report, in 1QFY26, 4QFY25, DRAM contributed to 34% of its total semiconductor systems sales, rising from 28% in 4QFY25.

Applied Materials highlighted its fastest-growing markets: in DRAM, 4F² and 3D DRAM lead the surge; in Advanced Packaging, HBM, hybrid bonding, and panel substrates are driving momentum. NAND growth comes from higher layer counts and tech transitions, while ICAPS focuses on compound semiconductors (SiC, GaN) and photonics, the company said.

Other major players are riding the memory boom as well. DRAM sales accounted for 23% of Lam Research’s December-quarter revenue, up from 16% in the previous quarter.

Tokyo Electron, on the other hand, shows a notable recovery in DRAM demand within its SPE new equipment sales. After DRAM’s share dipped to 26% in Q1 FY2026, it rebounded to 27% in Q2 and climbed further to 36% in Q3 FY2026.

Read more

(Photo credit: Applied Materials’ Facebook)

Please note that this article cites information from Reuters, Applied Materials, Lam Research and Tokyo Electron.