Popular Keywords

About TrendForce News

TrendForce News operates independently from our research team, curating key semiconductor and tech updates to support timely, informed decisions.

[News] Asia’s Chipmakers Reportedly Eye $136B Spend in 2026, Up 25% YoY, Spanning Foundry and Memory

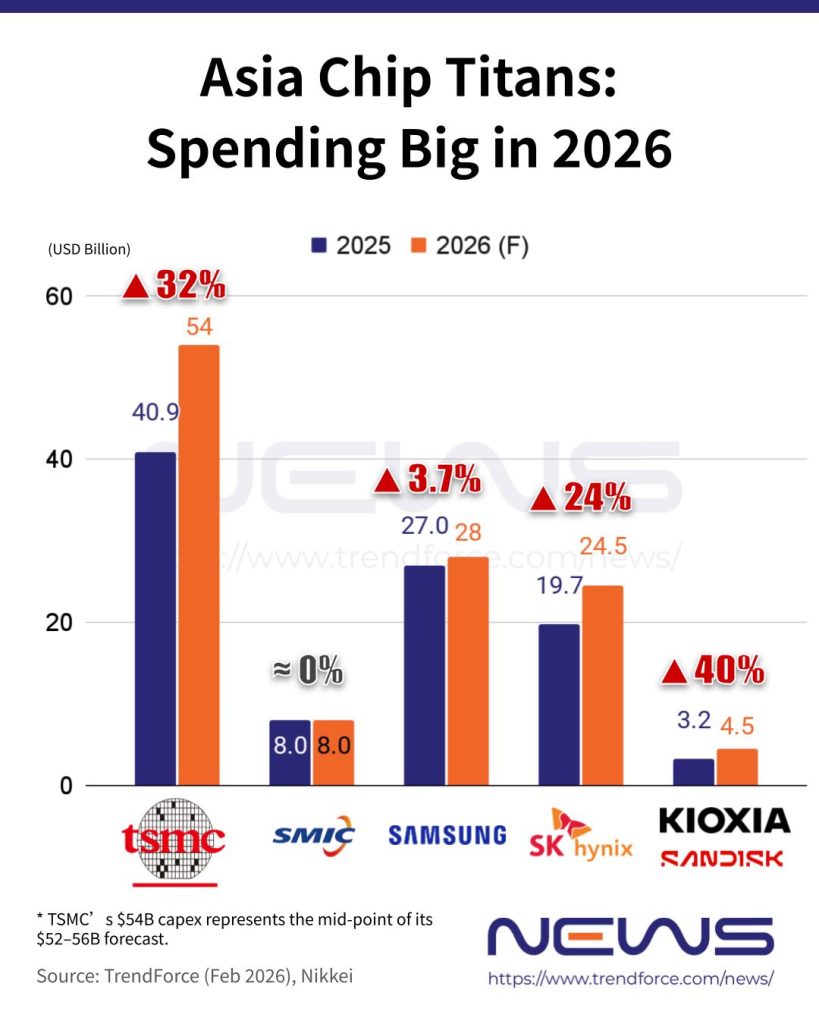

Fueled by soaring demand for AI chips, memory, and logic processors, Asia’s top chipmakers are ramping up their 2026 capital spending. Nikkei and TrendForce report that leading semiconductor firms across South Korea, Taiwan, Japan, and China plan to invest over $136 billion this year, a 25% increase from 2025, with giants like TSMC, Samsung, and SK hynix leading the charge.

Foundries Lead the 2026 Capex Surge

Foundry leaders and major memory players in Asia are ramping up their 2026 investments sharply. As previously reported by Commercial Times and Central News Agency, TSMC plans a record $52–56 billion in capex this year, a 27–37% increase, with 70–80% focused on advanced processes and the rest earmarked for specialty nodes and advanced packaging.

China’s top foundry, SMIC, is maintaining record capital spending nearly equal to its annual revenue, focusing primarily on domestic production, Nikkei notes. The Economic Daily News reports that its 2026 capex is expected to stay roughly flat versus 2025, remaining above $8 billion.

Memory Makers Expand Capacity, Focus on HBM

Meanwhile, Samsung and SK hynix are also ramping up 2026 investments, according to Nikkei and TrendForce’s projection. Samsung’s capex is projected to rise about 3.7% year-on-year, while SK hynix is expected to boost spending by 24%, reflecting the region’s ongoing semiconductor expansion.

According to South Korean media outlet EBN, both Samsung and SK hynix are expanding production capacity, but most of the added output is expected to go toward HBM. Samsung plans to increase DRAM output by about 20% in 2026, centered on its Pyeongtaek P4 plant, but the boost will primarily support 10nm 6th-generation (1C) DRAM for HBM4, the report explains.

On the other hand, the EBN report adds that SK hynix has also completed preparations at its Cheongju M15X plant, and a significant portion of the expanded capacity is expected to be allocated to HBM production.

The Elec reported in late January that SK hynix has revised upward its expansion plan for 1C DRAM production. Industry sources cited by the report estimated the company’s monthly output could reach 170,000–200,000 units by the end of Q1 2027, nearly doubling the original target of 90,000 units per month.

In addition, the Kioxia–SanDisk alliance is emerging as one of the most aggressive spenders in the NAND sector. Citing TrendForce projects that the joint venture’s 2026 capex could surge by as much as 40%, signaling a strong push to expand NAND capacity.

Second-Tier Memory Makers Step Up 2026 Investments

Notably, the spending wave is extending beyond industry heavyweights to second-tier memory makers. Nikkei reports that Taiwan’s specialty memory supplier Winbond Electronics plans to invest NT$42.1 billion in 2026 — nearly eight times last year’s outlay.

Known for its niche NOR flash chips used to store source code in a wide range of devices, as well as legacy customized DRAM, Winbond also expects its average selling prices to climb more than 30% in Q1 2026, Nikkei notes.

Nanya Technology, the world’s fifth-largest DRAM maker, announced it will more than double its 2026 capital spending after nearly three years of a sharp market downturn, Nikkei reports. According to TechNews, Nanya Tech has announced a record NT$50 billion capital expenditure budget for 2026, with the new plant expected to reach 20,000 wafers per month in the first half of 2028.

Read more

- [News] Samsung & SK hynix Earnings Showdown on 1/29: Profit, CAPEX, HBM4 in Focus

- [News] TSMC Advanced Packaging CapEx Projected to Grow 24% CAGR in 2025–27; AP7 Eyes WMCM, CoPoS

(Photo credit: SK hynix)

Please note that this article cites information from Nikkei, Commercial Times, Central News Agency, Economic Daily News, EBN, The Elec and TechNews.