Popular Keywords

About TrendForce News

TrendForce News operates independently from our research team, curating key semiconductor and tech updates to support timely, informed decisions.

[News] Memory Makers Reportedly Halt Quotes on Select DRAM, NAND Products as China Faces “Daily Pricing”

With South Korean DRAM giants reportedly hiking prices by up to 30% recently, China’s memory market is feeling intense pressure. According to Commercial Times, citing Calian Press, some manufacturers have even halted quotations for certain DRAM and NAND flash products, and when prices are quoted, they’re valid for such brief periods that they essentially change on a daily basis.

As per Calian, the pricing pressure has reached even major tech players, with Xiaomi founder Lei Jun acknowledging on Weibo on October 24th that memory prices have surged substantially in recent months.

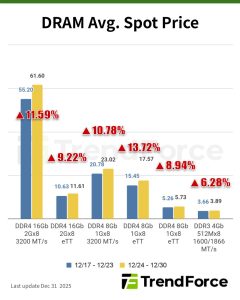

The price pressure is evident across the board. Multiple Chinese module makers told Cailian Press that DDR4 prices from manufacturers have been climbing steadily since Q1. Market data from Manmanbuy App reportedly shows the impact: a Kingston DDR4 desktop memory module that began surging in March now costs more than double its price from a year ago, the report adds.

Price Hike Rally to Continue

In context, TrendForce reports that since HBM consumes over three times the wafer capacity of standard DRAM, memory giants are prioritizing production of higher-margin HBM and DDR5, squeezing supply of legacy products like DDR4 and LPDDR4X used in consumer electronics.

Thus, TrendForce, cited by Cailian Press, projects that DDR4 shortages could extend into the first half of 2026, while overall DRAM prices (including HBM) are expected to climb 13%-18% quarter-over-quarter in Q4.

AI Demand and Capacity Constraints Fuel Prolonged Price Surge

Calian Press suggests that the memory industry is notoriously cyclical, with sharp rises typically followed by downturns. Yet this year, memory chip prices have reportedly climbed for over six months, and far from cooling in the fourth quarter, the surge has intensified due to multiple overlapping factors.

TrendForce identifies two distinct drivers behind the price surge: Q2-Q3 2025 increases stemmed from DDR4 end-of-life announcements and pre-emptive stockpiling amid U.S.-China tariff tensions. From Q4 2025 through H1 2026, further hikes are expected as North American data centers accelerate AI server investments, driving demand for DDR5 RDIMM, LPDDR5X, and HBM.

With capacity expansion lagging behind demand, supply shortages for mature-node products are set to intensify, TrendForce notes.

Regarding China’s domestic players, Cailian Press, citing TrendForce, reports that since August the industry has entered a fresh round of price increases. Manufacturers have seen profits expand significantly, while module makers have been actively stockpiling chip and wafer inventories, the report adds.

Read more

- [News] Samsung, SK hynix Reportedly Lift Memory Prices Up to 30%; Long-Term Supply Deals in Play

- [News] Samsung Reportedly Plans Q4 Memory Price Hikes: DRAM Up 30%, NAND Up 10%

(Photo credit: Samsung)

Please note that this article cites information from Calian Press, Commercial Times and Lei Jun’s Weibo.