Google's Data Center Interconnect Architecture: Rise of 800G+ Optical Modules and 2026 Supply Chain Outlook

Last Modified

2026-02-26

Update Frequency

Not

Format

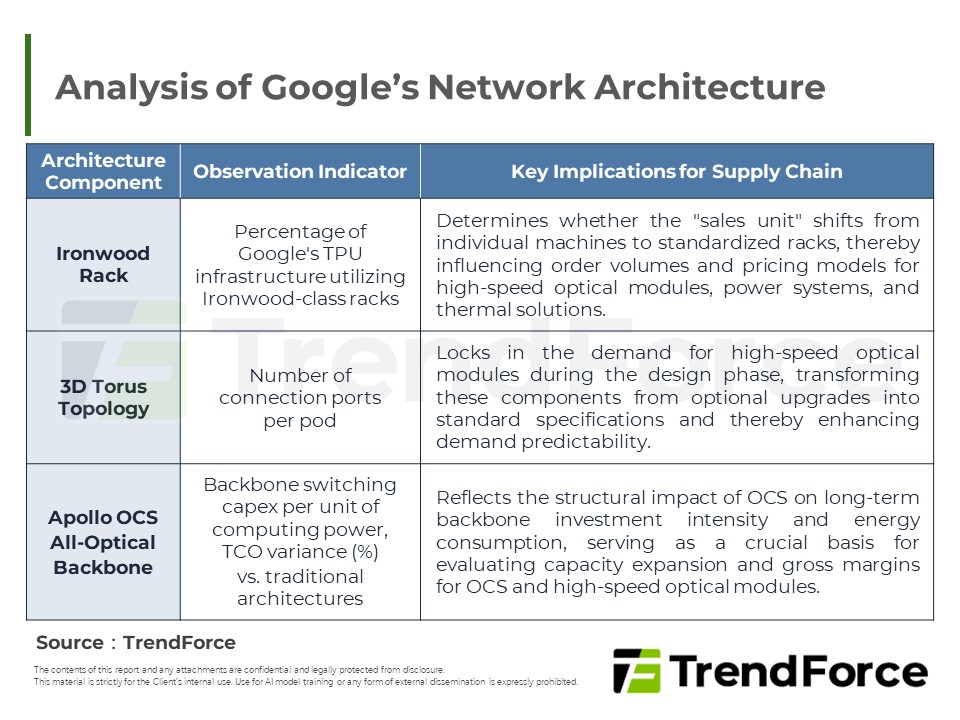

1. Google is consolidating its proprietary TPUs, Ironwood racks, 3D Torus topology, and the Apollo OCS optical backbone into a unified high-speed interconnect architecture. As a result, the focus of cluster planning is shifting from individual servers to modular designs centered on racks and Superpods.

2. Under this architecture, the share of 800G+ high-speed optical modules in data centers deployments is projected to grow from roughly 20% in 2024 to over 60% by 2026. No longer an optional upgrade, these modules are becoming the baseline configuration for next-generation clusters, driving annual demand into the millions.

3. For the optical interconnect supply chain, 800G+ optical modules and OCS systems are becoming critical elements deeply integrated with Google’s infrastructure. Between 2026 and 2028, supply tightness and profitability within the sector will be primarily driven by the available production capacity and yield rates of lasers and MEMS.

4. For industry strategists and investors, assessing the market outlook over the coming years requires looking beyond GPU and TPU shipments. It is equally important to track the shipment volume and penetration of 800G/1.6T optical modules to fully understand the structural shifts between computing power deployment and high-speed interconnect investments.

Key Highlights

- Google integrates TPUs, Ironwood racks, 3D Torus topology, and Apollo OCS into a unified high-speed interconnect, shifting cluster planning from server-centric to rack- and Superpod-centric modular designs.

- High-speed optical modules (800G+) see rising deployment in data centers, evolving from optional to essential baseline for next-gen clusters, fueling massive demand.

- Optical interconnect supply chain emphasizes 800G+ modules and OCS as core to Google's infrastructure; future tightness and profitability hinge on laser and MEMS production capacity and yields.

- Strategists and investors should track 800G/1.6T module shipments and penetration beyond GPU/TPU volumes to grasp shifts in computing power and interconnect investments.

Table of Contents

- Google: From In-House Compute User to Architect of High-Speed Interconnects

- Two primary ways this architectural shift is reshaping the high-speed optical module market

- Figure 1: 2024~2026 Global Transceiver Shipments

- Figure 2: 2026 >800G Transceiver Shipment & Google TPU Shipment

- Google Fabric Architecture

- Figure 3: Ironwood TPU Fabric

- Figure 4: 3D Torus & Apollo OCS

- Table 1: Analysis of Google’s Network Architecture

- High‑Speed Optics & Supply Chain Dynamics

- Scenario Analysis

- Table 2: Bear/Base/Bull Scenarios for Annual TPU Shipments in 2026

- Table 3: Impact of Bear/Base/Bull Scenarios on Architecture, Supply Chain, and Technology

- TRI’s View

<Total Pages: 14>

Category: Telecommunications

Spotlight Report

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Selected Topics

PDF

-

Mature Memory Structural Shortage: Price Plateau Era Arrives - 2H26

2026/06/02

Selected Topics

PDF

-

Cascading Shortages in Consumer DRAM: How Capacity Pivots Fuel Legacy Node Adoption

2026/06/17

Selected Topics

PDF

-

SLC NAND Price Surge: Global Capacity Gap & Substitution Wave in 2H 2026

2026/07/06

Selected Topics

PDF

-

AI Wave & DRAM Deficits: 2027 Global DRAM Outlook

2026/07/28

Selected Topics

PDF

-

HBM Market Outlook:HBM Suppliers Seize Pricing Power as AI Demand Fuels Explosive Contract Price Surge

2026/05/27

Selected Topics

PDF

Selected TopicsRelated Reports

Download Report

2,500

Membership

- Selected Topics New

- Selected Topics-173_Analysis of Google’s High-Speed Interconnect Architecture: The Rise of 800G+ Optical Modules and the 2026 Penetration and Supply Chain Outlook

Spotlight Report

-

AI Servers Absorbing LPDRAM Capacity, Signaling Tight Supply as the New Norm

2026/06/05

Selected Topics

PDF

-

Mature Memory Structural Shortage: Price Plateau Era Arrives - 2H26

2026/06/02

Selected Topics

PDF

-

Cascading Shortages in Consumer DRAM: How Capacity Pivots Fuel Legacy Node Adoption

2026/06/17

Selected Topics

PDF

-

SLC NAND Price Surge: Global Capacity Gap & Substitution Wave in 2H 2026

2026/07/06

Selected Topics

PDF

-

AI Wave & DRAM Deficits: 2027 Global DRAM Outlook

2026/07/28

Selected Topics

PDF

-

HBM Market Outlook:HBM Suppliers Seize Pricing Power as AI Demand Fuels Explosive Contract Price Surge

2026/05/27

Selected Topics

PDF