HBM Industry Analysis - 4Q25

Last Modified

2025-10-31

Update Frequency

Quarterly

Format

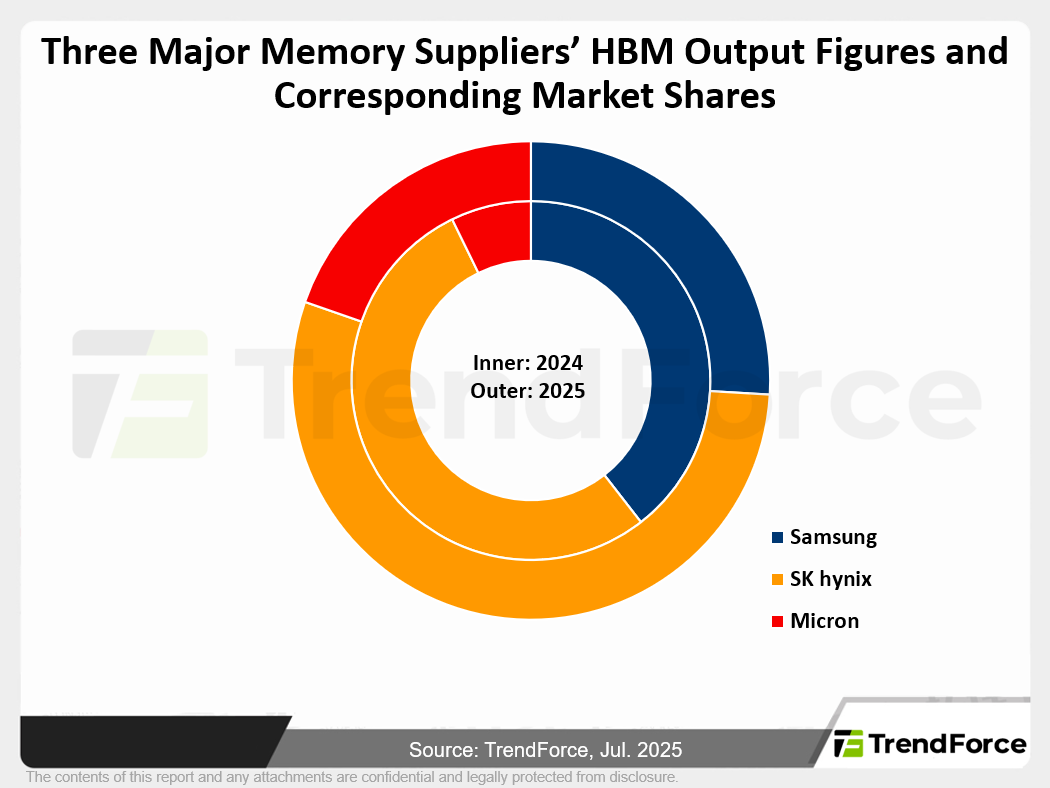

Major suppliers are expanding HBM capacity, with 2025 shipments revised upward. SK hynix leads with 150K TSV capacity, while Micron ramps up its Taiwan facilities. By 2026, all three will begin HBM4 mass production, with Samsung's shipment growth expected to lead.

Key Highlights

- AI chip demand favors next‑gen high‑stack HBM and supplier product shifts.

- Yield and certification constrain near‑term supply; back‑end capacity buildout is critical.

- NVIDIA raised HBM4 specifications, and after suppliers resubmitted samples, the 2026 procurement share remains uncertain.

Table of Contents

- Introduction

- Memory Suppliers' Figures for HBM Output and TSV Processing Capacity

- Three Major Memory Suppliers' HBM Output Figures and Corresponding Market Shares

- Analysis of HBM Generations and Die Stack Levels

- Updates on New Backend Packaging and Testing Facilities

- Analysis of HBM Demand

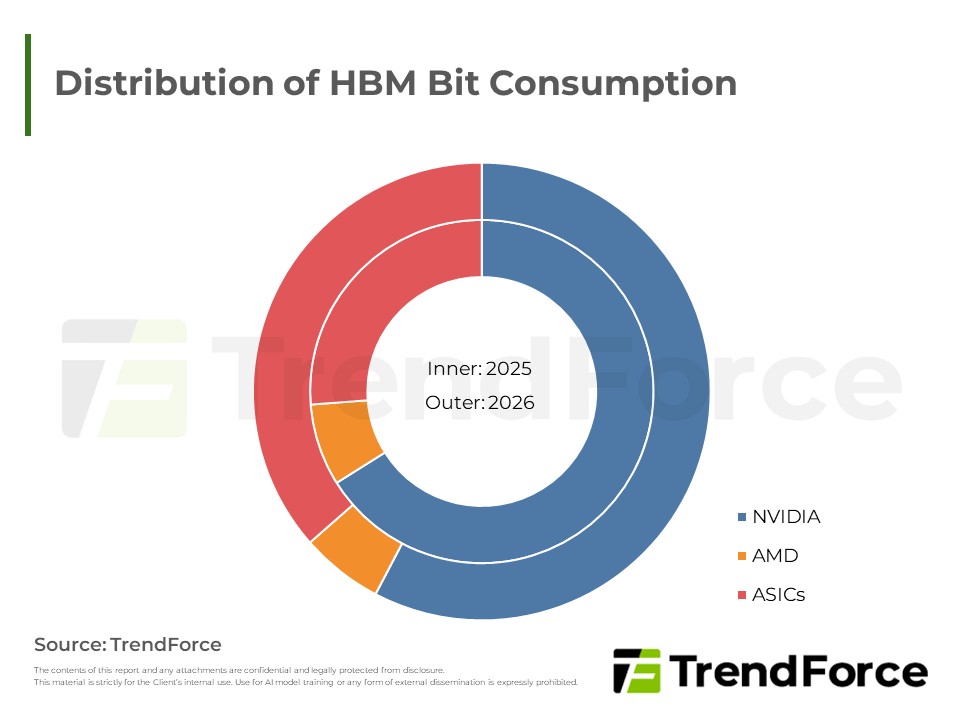

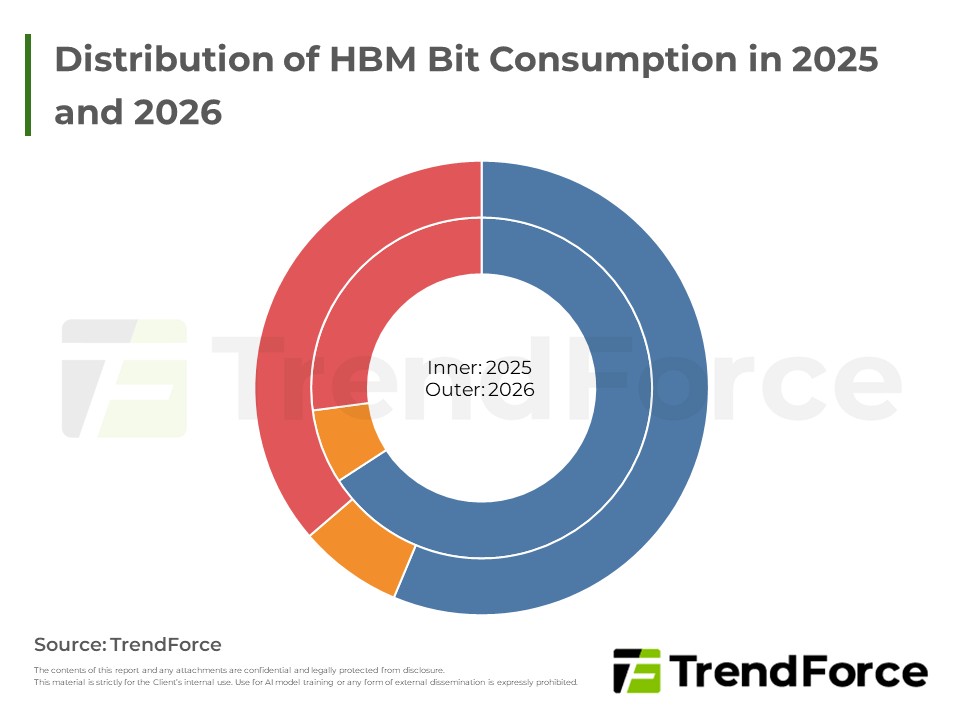

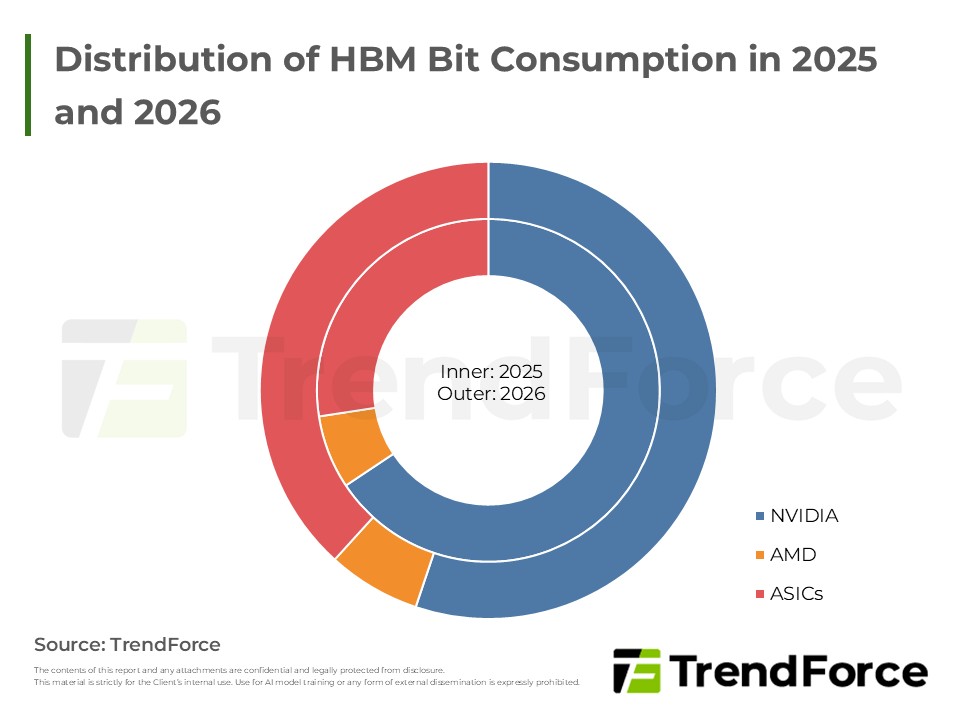

- Distribution of HBM Bit Consumption in 2025 and 2026

- HBM S/D Ratio

- HBM S/D Ratio

- Analysis on Prices and Revenue of HBM

- Blended ASP of HBM

- Revenue Share of HBM Products

- Revenue Share of HBM Suppliers

<Total Pages: 17>

Category: AI/HBM/Server

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

2Q26 Memory Price Forecast

2026/03/26

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

DRAM Contract Price Mar. 2026

2026/03/31

Semiconductors

PDF

HBM Quarterly ReportRelated Reports

Download Report

30,000

Membership

Spotlight Report

-

DRAM Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

EXCEL

-

NAND Flash Monthly Datasheet Jun. 2026

2026/06/16

Semiconductors

PDF

-

2Q26 Memory Price Forecast

2026/03/26

Semiconductors

PDF

-

DRAM Contract Price May 2026

2026/05/29

Semiconductors

PDF

-

DRAM Contract Price Apr. 2026

2026/04/30

Semiconductors

PDF

-

DRAM Contract Price Mar. 2026

2026/03/31

Semiconductors

PDF